Main risks and uncertainties to which Reply S.p.A and the group are exposed

The Reply Group adopts specific procedures in managing risk factors that can have an influence on company results. Such procedures are a result of an enterprise management that has always aimed at maximizing value for its stakeholders putting into place all necessary measures to prevent risks related to the Group activities.

Reply S.p.A., as Parent Company, is exposed to the same risks and uncertainties as those to which the Group is exposed, and which are listed below.

The risk factors described in the paragraphs below must be jointly read with the other information disclosed in the Annual Report.

External risks

Risks associated with general economic conditions

The informatics consultancy market is strictly related to the economic trend of industrialized countries where the demand for highly innovative products is greater. An unfavourable economic trend at a national and/or international level or high inflation could alter or reduce the growth of demand and consequently could have negative effects on the Group’s activities and on the Group’s economic, financial and earnings position.

The battle against the Covid-19 pandemic will continue to determine the evolution of the economy at least for the next months. The emergency, at the time this annual report, is still ongoing, with different trends in the countries where Reply is present. Its evolution will depend, to a large extent, on the effectiveness and speed of the vaccination plans that the various countries have begun to activate.

It should also be noted that Russia’s recent invasion of Ukraine creates uncertainties and tensions particularly within the Eurozone. Although the relative evolutions and impacts are still uncertain and difficult to assess, the intensification of war hostilities, ongoing geopolitical tensions and trade war, including the imposition of international economic sanctions against companies, banks and Russians, could have significant negative repercussions on the global, international and Italian economy, on the performance of the financial markets and on the energy sector.

Risks related to the evolution of ict-related services

The ICT consulting services sector in which the Group operates is characterised by rapid and profound technological changes and by a constant evolution of the mix of professional skills and expertise to be pooled in the provision of the services themselves, with the need for continuous development and updating of new products and services, and a prompt go to market. Therefore, the future development of the Group’s activities will also depend on its ability to foresee technological developments and the content of its services, also through significant investments in research and development activities, or through effective and efficient extraordinary operations.

Risks associated with competition

The ICT market is highly competitive. Competitors could expand their market share squeezing out and consequently reduce the Group’s market share. Moreover the intensification of the level of competition is also linked with possible entry of new entities endowed with human resources and financial and technological capacities in the Group’s reference sectors, offering largely competitive prices which could condition the Group’s activities and the possibility of consolidating or amplifying its own competitive position in the reference sectors, with consequent repercussions on business and on the Group’s economic, earnings and financial situation.

Risks associated with changes in client needs

The Group’s solutions are subject to rapid technological changes which, together with the growing or changing needs of customers and their own need for digitalisation, could translate into requests for the development of increasingly complex activities that sometimes require excessive commitments that are not economically proportionate, or could result in the cancellation, modification or postponement of existing contracts. This could, in some cases, have repercussions on the Group’s business and on its economic and financial situation.

Risks associated with segment regulations

The Group is subject to the laws and regulations applicable in the countries in which it operates, such as, among the main ones, regulations on the protection of occupational health and safety, the environment and the protection of intellectual property rights, tax regulations, regulations on the protection of privacy, the administrative liability of entities pursuant to Legislative Decree No. 231/01 and responsibilities under Law 262/05.

The Group operates in accordance with applicable legal requirements and has established processes to ensure that it is aware of the specific local regulations in the areas in which it operates and of regulatory changes as they occur.

Violations of these regulations could result in civil, tax, administrative and criminal sanctions, as well as the obligation to carry out regularisation activities, the costs and responsibilities of which could adversely affect the Group’s business and its results.

Risks related to the pandemic

The evolving Coronavirus pandemic linked to the spread of SARS-CoV-19 and the emergence of new Coronavirus strains, if not adequately contained, may continue to have significant health, social and economic consequences worldwide.

With regard to employees, for the purposes of emergency management, with the aim of protecting the health and safety of employees and external collaborators, task forces have been set up at Group and local level to monitor the evolution of the situation and ensure coordinated action on the measures to be implemented:

remote working was foreseen, where possible based on the type of work, and extended to all employees during the emergency phase;

all events involving a gathering of people were held virtually;

rules for access to company premises and measures to limit the risk of virus spread were established.

Pandemic risk management impacts the normal execution of processes, both internal and managed through external providers. For the management of the crisis resulting from Covid-19, ad hoc measures were put in place to ensure the continuity of operational processes. In particular, the IT infrastructure was adapted to support the mass use of secure remote working.

Internal risks

Risks associated with key management and loss of know-how

The Group’s success is largely due to certain key figures who have contributed in a decisive way to its development, such as the Chairman, the Chief Executive Officer and the executive directors of the Parent Company Reply S.p.A.. Reply also has a management team with many years of experience in the sector, which plays a decisive role in the management of the Group’s activities. The loss of the services of one of the aforementioned key figures without adequate replacement, as well as the inability to attract and retain new and qualified personnel, could have a negative impact on the Group’s prospects, maintenance of critical know-how, activities and economic and financial results. The Management believes, in any event, that the Company has an operational and managerial structure capable of ensuring continuity in the management of corporate affairs.

Risks associated with relationship with client

The Group offers consulting services mainly to medium and large size companies operating in different market segments (Telco, Manufacturing, Finance, etc.).

A significant part of the Group’s revenues, although in a decreasing fashion in the past years, is concentrated on a relatively limited number of clients. If such clients were lost this could have an adverse effect on the Group’s activities and on the Group’s economic, financial and earnings position.

Risks associated with internationalization

The Group, with an internationalization strategy, could be exposed to typical risks deriving from the execution of its activities on an international level, such as changes in the political, macro-economic, fiscal and/or normative field, along with fluctuations in exchange rates.

These could negatively influence the Group’s growth expectations abroad.

Risks related to group development

The constant growth in the size of the Group presents new management and organisational challenges.

The Group constantly focuses its efforts on training employees and maintaining internal controls to prevent possible misconduct (such as misuse or non-compliance with laws or regulations on the protection of sensitive or confidential information and/or inappropriate use of social networking sites that could lead to breaches of confidentiality, unauthorised disclosure of confidential company information or damage to reputation).

If the Group does not continue to make the appropriate changes to its operating model as needs and size change, if it does not successfully implement the changes, and if it does not continue to develop and implement the right processes and tools to manage the business and instil its culture and core values in its employees, the ability to compete successfully and achieve its business goals could be compromised.

Risks related to acquisitions and other extraordinary operations

The Group plans to continue to pursue strategic acquisitions and investments to improve and add new expertise, service offerings and solutions, and to enable expansion into certain geographic areas and other markets.

Any investment made as part of strategic acquisitions and any other future investment in Italian or international companies may involve an increase in complexity in the Group’s operations and there is no guarantee that such investments will generate the expected return on the acquisition or investment decision and that they will be properly integrated in terms of quality standards, policies and procedures in a manner consistent with the rest of the Group’s operations. The integration process may require additional costs and investments. Inadequate management or supervision of the investment made may adversely affect the business, operating results and financial matters.

Risks related to non-fulfilment of contractual commitments

The Group develops high-tech, high-value solutions; the underlying contracts, which may involve both internal staff and external contractors, may provide for the application of penalties for failure to meet agreed deadlines and quality standards. The application of such penalties could have negative effects on the Group’s economic and financial results and reputation. However, the Group has taken out insurance policies, deemed adequate, to protect itself against risks arising from professional liability for an aggregate annual maximum amount deemed adequate in relation to the underlying risk. However, if the insurance coverage is inadequate and the Group is required to pay damages in excess of the maximum amount provided, the Group’s financial position, results of operations and cash flows could be materially adversely affected.

Risks related to key partnerships

In order to offer the most suitable solutions to differing customer needs, the Group has established important partnerships with leading global vendors.

The business that the Group conducts through these partnerships may decline or not grow for a number of reasons, as the priorities and objectives of technology partners may differ from those of the Group and they are not prohibited from competing with the Group or entering into closer agreements with its competitors. Decisions the Group makes with respect to a technology partner may affect the ongoing relationship. In addition, technology partners may experience reduced demand for their technology or software, which could decrease the related demand for the Group’s services and solutions.

The risk of failing to adequately manage and successfully develop relationships with key partners, or of failing to foresee and establish effective alliances in relation to new technologies, could adversely affect the ability to differentiate services, offer cutting-edge solutions to customers or compete effectively in the market, with possible consequent repercussions on the business and on the economic and financial situation.

Risks related to the protection of intellectual property rights

The Group’s success depends, in part, on its ability to obtain intellectual property protection for its proprietary platforms, methodologies, processes, software and other solutions.

The Group relies on a combination of confidentiality, non-disclosure and other contractual agreements, and patent, trade secret, copyright and trademark laws and procedures to protect its intellectual property rights. Even where we obtain intellectual property protection, the Group’s intellectual property rights cannot prevent or discourage competitors, former employees or other third parties from reverse engineering their own solutions or proprietary methodologies and processes or independently developing similar or duplicate services or solutions.

In addition, the Group may unwittingly infringe the rights of others and be liable for damages as a result. Any claims or litigation in this area could cost time and money and lead to damage the Group’s reputation and/or require it to incur additional costs to obtain the right to continue offering a service or solution to its customers.

The occurrence of such risks could adversely affect the Group’s competitive advantage and market positioning, its economic, financial and capital position, as well as its reputation and prospects for future business development.

Cyber security, data management and dissemination risks

The Group’s business relies on IT networks and systems to process, transmit and store electronic information securely and to communicate with its employees, customers, technology partners and suppliers. As the scale and complexity of this infrastructure continues to grow, not least due to the increasing reliance on and use of mobile technologies, social media and cloud-based services, and as increasingly more of our employees are working remotely during the coronavirus pandemic, the risk of security incidents and cyber-attacks increases. Such breaches could result in the shutdown or disruption of the Group’s systems and those of our customers, technology partners and suppliers, and the potential unauthorised disclosure of sensitive or confidential information, including personal data.

In the event of such actions, the Group could be exposed to potential liability, litigation and regulatory or other actions, as well as loss of existing or potential customers, damage to brand and reputation, and other financial losses. In addition, the costs and operational consequences of responding to violations and implementing corrective measures could be significant.

To date, there hasn’t been a cybersecurity attack that has had a material effect on the Group, although there is no guarantee that there won’t be a material impact in the future. As the business and cyber security landscape evolves, the Group may also find it necessary to make significant additional investments to protect data and infrastructure.

However, if the insurance coverage, which includes IT insurance, is inadequate and the Group is required to pay damages in excess of the maximum amount provided, the Group’s financial position, results of operations and cash flows could be materially adversely affected.

Risks in terms of social and environmental responsibility and business ethics

In recent years, the growing community focus on social, environmental and business ethics issues, as well as the evolution of national and international regulations, have given impetus to the disclosure and measurement of non-financial performance, which is now fully included among the qualifying factors of corporate management and competitive capacity of a company.

In this regard, socio-environmental issues and business ethics are increasingly integrated into the strategic choices of companies and are increasingly attracting the attention of various stakeholders concerned with sustainability issues.

The Group is committed to managing its business activities with a particular focus on respect for the environment, social issues, labour relations, the promotion of human rights and the fight against corruption, contributing to the spread of a culture of sustainability in respect of future generations.

Failure to adequately address these issues could subject the Group to risks of sanctions as well as reputational risks.

For a more specific discussion of sustainability/ESG risks, please refer to the Disclosure of Non-Financial Information (NFI), published on the Reply website in the Investor Corporate Governance section.

Financial risks

Credit risk

For business purposes, specific policies are adopted to assure its clients’ solvency.

With regards to financial counterparty risk, the Group does not present significant risk in credit-worthiness or solvency.

The Group’s exposure to credit risk is the potential losses that could result from non-fulfilment of the obligations assumed by both commercial and financial counterparties. In order to measure this risk over time, as part of the impairment of its financial assets (including trade receivables), the Group has applied a model based on expected credit losses pursuant to IFRS.

This exposure is mainly due to general economic and financial items, the possibility of specific insolvency situations of some debtor counterparties and more strictly technical-commercial or administrative elements.

The maximum theoretical exposure to credit risk for the Group is the book value of financial assets and trade receivables. The risk related to trade receivables is managed through the application of specific policies aimed to ensure the solvency of customers.

Provisions to the allowance for doubtful accounts are made specifically on creditor positions with specific risk elements. On creditor positions which do not have such characteristics, provisions are made on the basis of the average default estimated on the basis of statistical indicators.

Liquidity risk

The group is exposed to funding risk if there is difficulty in obtaining finance for operations at any given point in time.

The cash flows, funding requirements and liquidity of the Group’s companies are monitored or centrally managed under the control of the Group Treasury, with the objective of guaranteeing effective and efficient management of capital resources (maintaining an adequate level of liquid assets and funds obtainable via an appropriate committed credit line amount).

The difficult economic and financial context of the markets requires specific attention as regards the management of liquidity risk and in such a way that particular attention is given to shares tending to generate financial resources with operational management and to maintaining an adequate level of liquid assets. The Group therefore plans to meet its requirements to settle financial liabilities as they fall due and to cover expected capital expenditures by using cash flows from operations and available liquidity, renewing or refinancing bank loans.

Exchange rate and interest rate risk

The Group entered into most of its financial instruments in Euros, which is its functional and presentation currency. Although it operates in an international environment, it has a limited exposure to fluctuations in the exchange rates.

The exposure to interest rate risk arises from the need to fund operating activities and M&A investments, as well as the necessity to deploy available liquidity. Changes in market interest rates may have the effect of either increasing or decreasing the Group’s net profit/(loss), thereby indirectly affecting the costs and returns of financing and investing transactions.

The interest rate risk to which the Group is exposed mainly derives from bank loans; to mitigate such risks, the Group, when necessary, has used derivative financial instruments designated as “cash flow hedges“.

The use of such instruments is disciplined by written procedures in line with the Group’s risk management strategies that do not contemplate derivative financial instruments for trading purposes.

Tax risk

The risk of any changes in tax law and its application or interpretation could have a negative or positive impact on the Group’s results of operations, affecting the effective tax rate.

The Company adheres to the National Tax Consolidation scheme pursuant to articles 117/129 of the Consolidated Income Tax Act (TUIR). Reply S.p.A., the Parent Company, acts as consolidating company and determines a single taxable income for the Group of companies participating in the Tax Consolidation, benefiting from the possibility of offsetting taxable income with tax losses in a single declaration. The tax risk limitation measures put in place by Management, in terms of verifying the adequacy and correctness of tax compliance, obviously cannot completely exclude the risk of tax audits.

Review of the group’s economic and financial position

Foreword

The financial statements commented on and illustrated in the following pages have been prepared on the basis of the Consolidated financial statements as at 31 December 2021 to which reference should be made, prepared in compliance with the International Financial Reporting Standards (“IFRS“) issued by the International Accounting Standards Board (“IASB“) and adopted by the European Union, as well as with the provisions implementing Article 9 of Legislative Decree No. 38/2005.

Trend of the period

The Reply Group closed 2021 with a consolidated turnover of €1,483.8 million, an increase of 18.7% compared to €1,250.2 million in 2020

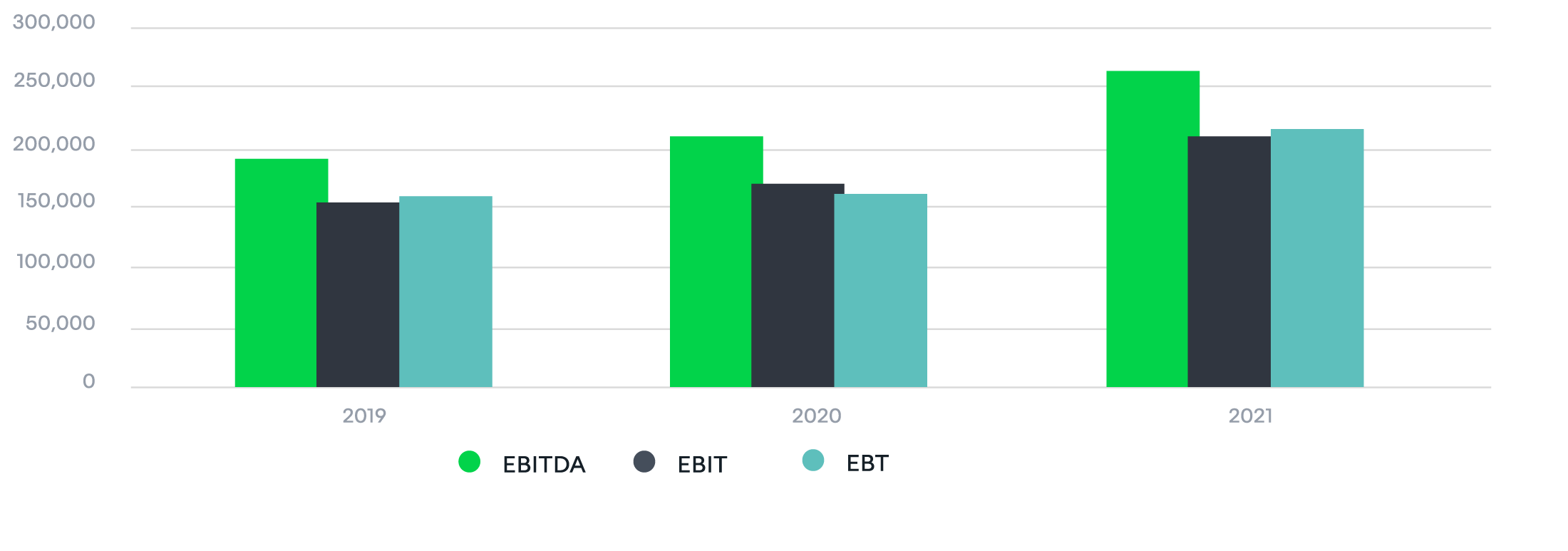

All indicators are positive for the period. Consolidated EBITDA was €262.8 million, an increase of 26.4% compared to €207.9 million recorded in 2020.

EBIT, from January to December, was at €209.3 million, which is an increase of 23.4% compared to € 169.5 million in 2020.

The Group net profit was at €150.7 million, an increase of 21.9% compared to the €123.6 million recorded in 2020.

As at 31 December 2021, the Group’s net financial managerial position has been positive, at €193.2 million. As at 30 September 2021, the net financial managerial position was positive, at €244.4 million.

2021 was a very good year for the Group, both in terms of revenue and margin growth. In recent months, Reply has continued to invest, gaining additional market share in Europe, England and North America, and has added new components to the leading solutions in cloud computing, artificial intelligence, robotics and connected vehicles.

Today, Reply combines a solid financial position with a wealth of unique expertise on the market, and top-quality execution and delivery skills.

For the moment, the future is still uncertain: while the health emergency currently seems to be under control in the countries where Reply operates, the recent outbreak of war on Europe’s eastern borders has exacerbated signs of stress in all the main markets, with medium and long-term consequences that are difficult to anticipate.

In any case, the process of transformation towards a new digital economy that started in 2020 is now unstoppable and has opened up ample opportunities for growth and development for companies like ours. High-speed communication software infrastructure, e-commerce, new digital experiments and rapid acceleration towards automation and green tech will be the building blocks of the economy over the coming years.

Reclassified consolidated income statement

Reply’s performance is shown in the following reclassified consolidated statement of income and is compared to corresponding figures of the previous year:

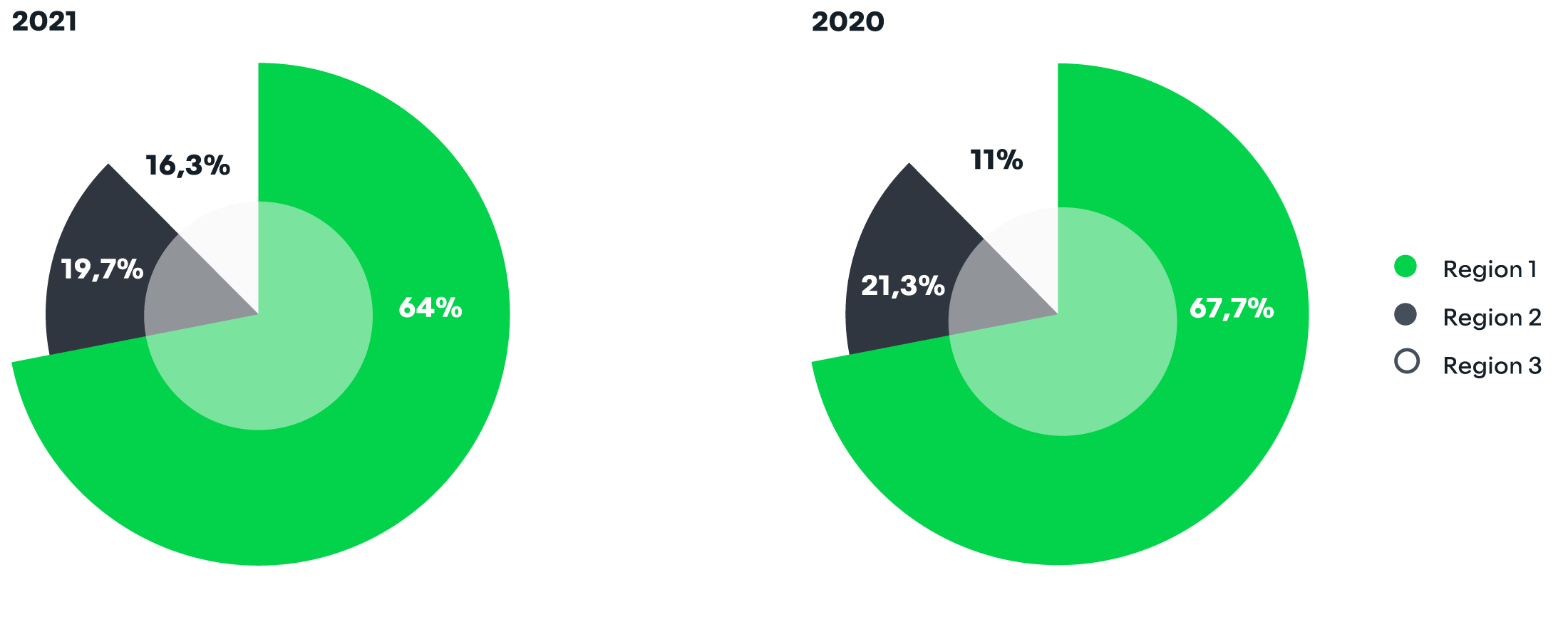

REVENUES BY REGION (*)

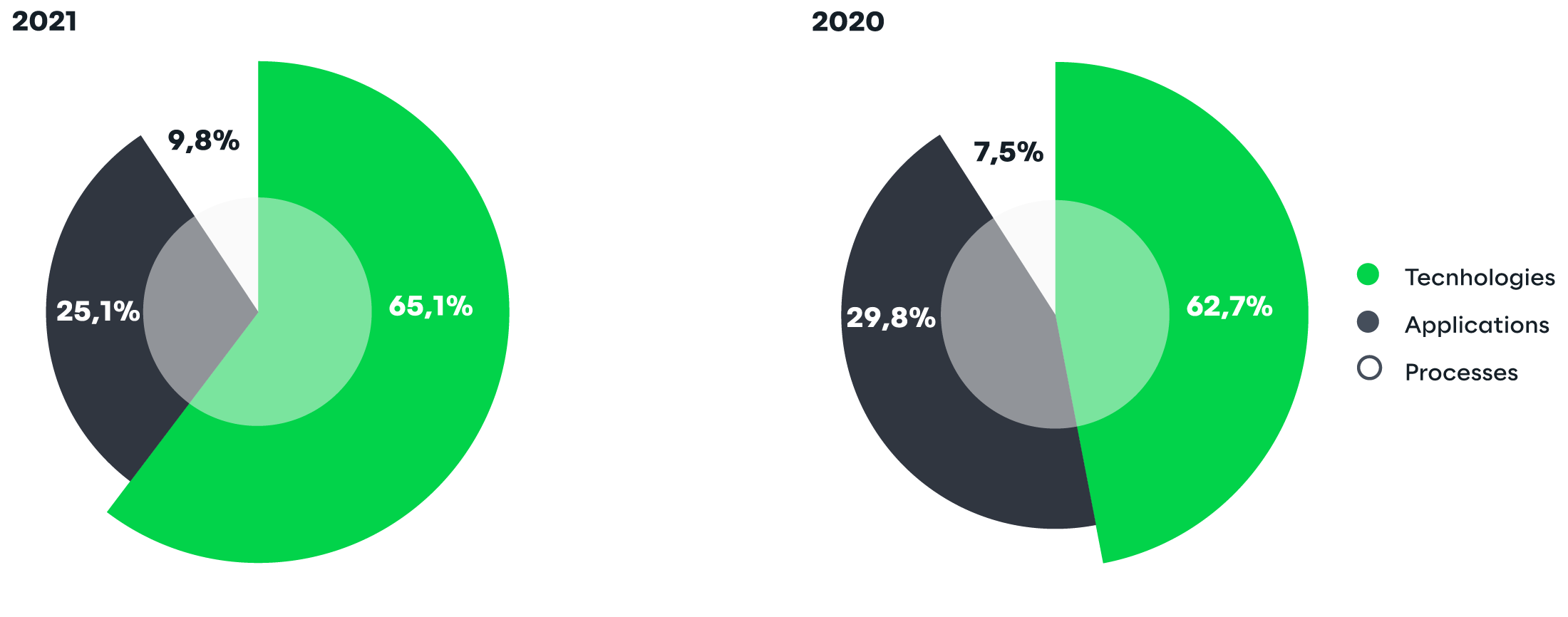

REVENUES BY BUSINESS LINES

TREND IN KEY ECONOMIC INDICATORS

Analysis of the financial structure

The Group’s financial structure is set forth below as at 31 December 2021, compared to 31 December 2020:

Net invested capital on 31 December 2021, amounting to 622,683 thousand Euros, was funded by Shareholders’ equity for 815,895 thousand Euros and by available overall funds of 193,212 thousand Euros.

It is to be noted that net invested capital includes Due to minority shareholders and Earn-out for a total of 129,558 thousand Euros (71,381 thousand Euros at 31 December 2020); this item is not included in the net financial managerial position. For the ESMA Net financial indebtedness see note 30.

The following table provides a breakdown of the net working capital:

Net financial managerial position and cash flows statement

Change in the item cash and cash equivalents is summarized in the table below:

The complete consolidated cash flow statement and the details of cash and other cash equivalents net are set forth in the financial statements.

Alternative performance indicators

In addition to conventional financial indicators required by IFRS, presented herein are some alternative performance measures, in order to allow a better understanding of the trend of economic and financial management.

These indicators, that are also presented in the periodical Interim management reports must not, however, be considered as replacements to the conventional indicators required by IFRS.

Set forth below are the alternative performance indicators used by the Group with relevant definition and basis of calculation:

EBIT: corresponds to the “Operating margin“

EBITDA: Earnings before interest, taxes, depreciation and amortization and is calculated by adding to the Operating margin the following captions:

EBT: corresponds to the Income before taxes

Net financial managerial position: rrepresents the financial structure indicator and is calculated by adding the following balance sheet captions:

Cash and cash equivalents

Financial assets (short-term)

Financial liabilities (long-term)

Financial liabilities (short-term)

Significant operations in 2021

Acquisition of Business Elements Group BV

On May 28, 2021, Reply Sarl acquired 100% of the share capital in Business Elements Group BV, a company established under Belgium law, for an initial consideration amounting to 3,628 thousand Euros. The company is specialized in consulting services and application development on the Microsoft Dynamics CRM platform.

Acquisition of Comwrap GmbH

On October 28, 2021, Reply SE acquired 100% of the share capital in Comwrap GmbH, a company established under Germany law, Europe leader in professional services for cloud-native digital platforms based on Adobe Experience Cloud and Ibexa DXP, for an initial consideration amounting to 9,560 thousand Euros.

Acquisition of G Force Demco Ltd

On 23 December, 2021, Reply Ltd. Acquired 100% of the share capital in G Force Demco Ltd Group (which holds Gray Matter and Forcology Ltd.) for an initial consideration amounting to 4,500 thousand Pounds. The companies are specialized in marketing strategies and solutions to develop B2B sales in the automotive industry and support customers in using the standard components of the Salesforce suite and provide solutions based primarily on configuration.

Acquisition of Enowa LLC

On December 27, 2021, Reply Inc. acquired 100% of the share capital in Enowa LLC, a company established under American law, specialized in consulting and solutions development SAP technology, for an initial consideration amounting to 35,225 thousand Dollars.

Enowa LLC, based in Philadelphia, is leader in cloud design and value-added services on SAP technology and counts among its customers some of the largest American groups active in the chemical, healthcare, energy and consumer services sectors.

Acquisition of The Spur Group

On 31 December, 2021, Reply Inc. acquired 100% of the share capital in The Spur Group, a company established under American law, leader in sales and marketing consulting, for an initial consideration amounting to 33,821 thousand Dollars.

The Spur Group, based in Bellevue (Seattle), works with leading Tech Giants and global brands, including Cisco, Microsoft, Rockwell Automation, Qlik and VMWare in defining go-to-market and digital positioning strategies, combining strategy, marketing, data analysis and operating models.

Reply on the stock market

Reply share performance

Even though shares have recently been in reverse gear due to the worsening pandemic situation, investors can look back on 2021 with satisfaction. The Euro Stoxx 600, for example, gained 20%, which is anything but a meagre performance. The fact that dividend stocks were the right choice in the past year becomes even clearer when one looks at the investment alternative, i.e. the interest rate market. The bond performance is particularly poor on a global scale. Government bonds have caused global investors a loss of almost 6%.

The first half of 2021 was dominated by the success of biotechnology and pharmaceutical companies, having been able to make effective Corona vaccines available in the fall of 2020.

Driven by the hope that the vaccination campaigns could overcome the pandemic and thus create the conditions for a normalization of social and economic life, share prices rose sharply, also thanks to the expectation of gigantic fiscal packages from governments. Consequently, a strong economic recovery had also set in, as shown by the substantial increase in profits of many companies.

But that was the end of the good part of the stock market year. Although the stock markets continued their record chase, the upward trend flattened out. A large number of interrelated negative factors put the brakes on the stock markets’ soaring performance.

For Reply 2021 was another excellent stock exchange year. Apart from a brief period of weakness at the beginning of March 2021 where the share reached its low-level for the year of EUR 92.50 the Reply share entered into a steady upwards trend which induced a price increase of 91% until beginning of September. Upcoming concerns about new virus variants and inflation levels then led to a phase of significant volatility increases. A sharp decline of the share price at the beginning of October was overcompensated, and the Reply share saw its maximum performance in the middle of November reaching its high-level for the year of EUR 185.50. This outperformance was not entirely maintained during the rest of the year, and the share closed the year with a value increase of 88%. The market capitalization of Reply reached a new record level of EUR 6.7 billion.

In January 2022 the Reply share joined the severe market turbulences in the wake of the corona mutant Omikron, inflation and interest rate turnaround. At the time of writing, Reply shares were trading 10.5% below their 2021 year-end value.

As well the relative performance of the Reply share was very strong in 2021. Throughout the year Reply outperformed all Italian indices (MIB: +23%, FTSE Italy STAR: +45%), all European sector indices, including the EuroSTOXX Technology (+37%), and the S&P 500/IT (+33%).

Taking December 6, 2000, the date of the Reply IPO, as a reference, the Italian main index MIB improved significantly in 2021 but is still at 60% of its starting. In the same period Reply increased its IPO value by nearly 4,400%. In 2021 Reply nearly doubled the value creation adding 2,085 percentage points to the out-performance versus the MIB.

The strong increase of the Reply share price induced significant improvements as at the index memberships. Since the third quarter 2021 Reply is part of the Euro STOXX 600 index and the FTSE Euro Mid index. In December 2021 Reply became part of the newly defined MIB ESG index, a blue-chip index for Italy dedicat-ed to ESG best practices, made operational by Euronext and Vigeo Eiris - Moody’s ESG Solutions.

Share liquidity

Following the very strong share price increases 2021 marked new records for the trading of the Reply share, regarding the counter value of all traded shares. The trading volume in the Reply share amounted to EUR 1.8 billion, an increase of 52% compared to the year before. The effects of the increased share price overcompensated the reduction of the number of shares traded, which fell by 17%.

Due to the strong upside development, the Reply share traded at a valuation premium, compared to the participants of the peer group, when profitability measures are taken into account. Enterprise value to EBITDA and enterprise value to EBIT at the end of 2021 were 40% higher than the average value of the peer group constituents. Measured upon revenue, Reply traded 27% above the average valuation of the peer group at the end of 2021.

Dividend

Performance-based compensation is an essential pillar of the partnership-oriented business model of Reply. Like employees the Reply shareholders shall - in form of dividends - participate in the sustainable operational performance of the group. Each year this principle is balanced with the need of internal financing to fund the investments of Reply (in new start-up companies, new technologies and potential acquisitions to further elaborate the Reply offering portfolio in Germany, UK, US, France as the strategic Reply regions). In 2021 Reply achieved earnings per share of EUR 4.03, an increase of 22.1% compared to 2020. For the financial year 2021 the corporate bodies of Reply propose to the shareholders’ meeting to approve the payment of a dividend of EUR 0.80 (dividend 2020: EUR 0.56). Referred to the share price of Reply at the end of 2020 this corresponds to a dividend yield of 0.45%. Assuming the approval of the shareholders’ meeting, Reply will pay to its shareholders a dividend sum of EUR 29.9 million. In 2020 EUR 21 million were distributed.

The subsequent table gives an overview on the main parameters of the Reply share and their substantial developments during the last 5 years.

The shareholders base

At the end of 2021 43% of the Reply shares were owned by the founders of Reply, institutional shareholders owned 40% while retail shareholders owned 17% of the shares. The institutional shareholders’ base of Reply saw some significant changes. US investors, the most important investor country in Reply, slightly increased their ownership in Reply to 26% of institutional holdings versus 23% in the previous year. UK investors increased significantly and now rank number 2, owning around 20% (2020: 6%). Also, Italian investors raised their positions to 20% of institutional holdings (2020: 16%). The Nordic investors reduced their position to 6.5% of the shares, coming from 12% in 2020.

According to the Shareholders’ Ledger, on the date of this report the shareholders that directly or indirectly, also through an intermediary person, trust companies and subsidiaries, hold stakes greater than 3% of the share capital having the right to vote are the following:

Analysts

In 2021, eight (8) analysts covered the Reply share on a regular base. The reduction by 1 analyst is due to a merger of 2 European banks. Because of the stellar share price development, the covering analysts took a more cautious position on Reply. 2 ratings remained on “outperform“ while 5 analysts took a “neutral“ stance on the share. One analyst saw an underperforming share price development. All Reply analysts on average in Jan. 2021 foresaw a target price of EUR 175.30.

Dialog with the capital markets

An active and open communication policy ensuring prompt and continuous information dissemination is a major component of the Reply IR strategy. In 2021 Reply maintained its high level of activities with the capital markets. During 27 conferences Reply actively explained its equity story. Due to the pandemic no roadshows were conducted. Especially with French investors the communication contacts were increased by 29%. In 2021 - unchanged to the previous year - 87% of the investor meetings were held virtually. 11 brokers were involved in the IR activities of Reply. In the Institutional Investor Survey 2021 Reply ranked third among the best IR teams of developed Europe Small and Mid-Cap Issuers.

The Parent Company Reply S.p.A.

Introduction

The tables presented and disclosed below were prepared on the basis of the financial statements as at 31 December 2021 to which reference should be made, prepared in accordance with the International Financial Reporting Standards (“IFRS“) issued by the International Accounting Standards Board (“IASB“) and endorsed by the European Union, as well as with the regulations implementing Article 9 of Legislative Decree No. 38/2005.

Reclassified income statement

The Parent Company Reply S.p.A. mainly carries out the operational co-ordination and the technical and quality management services for the Group companies as well as the administration, finance and marketing activities.

As at 31 December 2021 the Parent Company had 95 employees (93 employees in 2020).

Reply S.p.A. also carries out commercial fronting activities for some major customers, whereas delivery is carried out by the operational companies. The economic results achieved by the Company are therefore not representative of the Group’s overall economic trend and the performances of the markets in which it operates. Such activity is instead reflected in the item Pass-through revenues of the Income Statement set forth below.

The Parent Company’s income statement is summarized as follows:

Revenues from operating activities mainly refer to:

royalties on the Reply trademark for 44,180 thousand Euros (35,433 thousand Euros in the financial year 2020);

shared service activities in favour of its subsidiaries for 40,881 thousand Euros (33,777 thousand Euros in the financial year 2020);

management services for 13,323 thousand Euros (11,656 thousand Euros in the financial year 2020).

Operating income 2021 marked a positive result of 9,280 thousand Euros after having deducted write-downs and amortization expenses of 3,037 thousand Euros (of which 178 thousand Euros referred to tangible assets, 2,431 thousand Euros to intangible assets and 428 thousand Euros related to right of use assets arising from the adoption of IFRS 16).

Financial income amounted to 23,485 thousand Euros and included interest income on bank accounts for 7,936 thousand Euros, interest expenses for 1,107 thousand Euros mainly relating to financing for the M&A operations and the non-effective portion of the IRS for positive 1,148 thousand Euros. Such result also includes net positive exchange rate differences amounting to 15,547 thousand Euros.

Income from equity investments which amounted to 87,689 thousand Euros refers to dividends received from subsidiary companies in 2021.

Losses on equity investments refer to write-downs and losses reported in the year by some subsidiary companies that were considered to be unrecoverable.

Net income for the year ended 2021, amounted to 111,244 thousand Euros after income taxes of 8,888 thousand Euros.

Financial structure

Reply S.p.A.’s financial structure as at 31 December 2021, compared to that as at 31 December 2020, is provided below:

The net invested capital on 31 December 2021, amounting to 175,862 thousand Euros, was funded by Shareholders’ equity in the amount of 551,043 thousand Euros and by available overall funds of 375,181 thousand Euros.

Changes in balance sheet items are fully analysed and detailed in the explanatory notes to the financial statements.

Net financial managerial position

The Parent Company’s net financial managerial position as at 31 December 2021, compared to 31 December 2020, is detailed as follows:

Change in the net financial position is analysed and illustrated in the explanatory notes to the financial position.

Reconciliation of equity and profit for the year of the parent company

In accordance with Consob Communication no. DEM/6064293 dated 28 July 2006, Shareholders’ equity and the Parent Company’s result are reconciled below with the related consolidated amounts.

Corporate Governance

The Corporate Governance system adopted by Reply - issuer listed at Euronext Star Milan - adheres to the new Corporate Governance Code for Italian Listed Companies issued by Borsa Italiana S.p.A..

In compliance with regulatory obligations the annually drafted “Report on Corporate Governance and Ownership Structures“ contains a general description of the corporate governance system adopted by the Group, reporting information on ownership structures and compliance with the Code, including the main governance practices applied and the characteristics of the risk management and internal control system also with respect to the financial reporting process.

The aforementioned Report, related to 2021, is available on the website www.reply.com.

The Corporate Governance Code is available on the website of Borsa Italiana S.p.A.

https://www.borsaitaliana.it/comitato-corporate-governance/codice/2020.pdf.

Declaration of non-financial data

The company, in accordance with the provisions of article 5 (3) (b) of Legislative Decree No 254/2016, has prepared the consolidated declaration of a non-financial nature which constitutes a separate report. The consolidated declaration of non-financial data 2021, drafted in accordance with the “GRI Standards“ reporting standard, is available on the Group website www.reply.com.

Other information

Research and development activities

Reply offers high technology services and solutions in a market where innovation is of primary importance.

Reply considers research and continuous innovation a fundamental asset in supporting clients with the adoption of new technology.

Reply dedicates resources to Research and Development activities in order to project and define highly innovative products and services as well as possible applications of evolving technologies. In this context, Reply has developed of its own platforms.

Reply has important partnerships with major global vendors so as to offer the most suitable solutions to different company needs. Specifically, Reply boasts the highest level of certification amongst the technology leaders in the Enterprise sector.

Human resources

Human resources constitute a primary asset for Reply which bases its strategy on the quality of products and services and places continuous attention on the growth of personnel and in-depth examination of professional necessities with consequent definitions of needs and training courses.

The Reply Group is comprised of professionals originating from the best universities and polytechnics. The Group intends to continue investing in human resources by bonding special relations and collaboration with major universities with the scope of attracting highly qualified personnel.

The people who work at Reply are characterized by enthusiasm, expertise, methodology, team spirit, initiative, the capability of understanding the context they work in and of clearly communicating the solutions proposed. The capability of imagining, experimenting and studying new solutions enables more rapid and efficient innovation.

The group intends to maintain these distinctive features by increasing investments in training and collaboration with universities.

At the end of 2021 the Group had 10,579 employees compared to 9,059 in 2020.

General Data Protection Regulation (GDPR)

The governance model of the Group privacy policy reflects what is required by the existing code for the protection of personal data and the European Regulation 679/16 (GDPR).

Privacy fulfilments are managed uniformly at the Reply Group level in order to maintain adequate levels of internal coherence and to facilitate external relations, in particular with authorities, customers and suppliers.

To ensure compliance the Group has adopted a GDPR program which provides several activities including:

updating the Group privacy organizational model;

designation for each Region of a Data Protection Officer;

reorganization of the central Privacy & Security Team;

preparation of contact link with the DPO and the Privacy & Security Team through a central ticketing system;

updating of e-learning and induction material related to data protection content;

mandatory GDPR and ICT Security training at all business levels;

assessment of privacy and security of IT central services;

drafting of Records of the treatment activities;

development and dissemination of new fundamental processes for GDPR, updating of existing data protection policies, development and dissemination of guidelines and contractual templates for GDPR;

periodic internal audits on the Companies for the correct application of the GDPR requirements in the work for customers and in the engagements of suppliers.

Transactions with related parties and group companies

During the period, there were no transactions with related parties, including intergroup transactions, which qualified as unusual or atypical. Any related party transactions formed part of the normal business activities of companies in the Group. Such transactions are concluded at standard market terms for the nature of goods and/or services offered, these transactions took place in accordance with the internal procedures containing the rules aimed at ensuring transparency and fairness, under Consob Regulation 17221/2010.

The company in the notes to the financial statements and consolidated financial statements provides the information required pursuant to Art. 154-ter of the TUF [Consolidated Financial Act] as indicated by Consob Reg. no. 17221 of 12 March 2010 and subsequent Consob Resolution no. 17389 of June 23, 2010, indicating that there were no significant transactions concluded during the period as defined by Art. 4, paragraph 1, let a) of the aforementioned regulation that have significantly affected the Group’s financial or economic position. The information pursuant to Consob communication of 28 July 2006 are presented in the annexed tables herein.

Treasury shares

At the balance sheet date, the Parent Company holds 70,028 treasury shares amounting to 7,219,996 Euros, nominal value equal to 9,208 Euros; at the balance sheet item net equity, the company has posted an unavailable reserve for the same amount.

At the date of this report the Company does not hold shares of other holding companies.

Financial instruments

In relation to the use of financial instruments, the company has adopted a policy for risk management through the use of financial derivatives, with the scope of reducing the exposure to interest rate risks on financial loans.

Such financial instruments are considered as hedging instruments as they can be traced to the object being hedged (in terms of amount and expiry date).

In the notes to the financial statements more detail is provided to the above operations.

Events subsequent to 31 December 2021

Despite the complexity of the current situation, since the beginning of the year Reply has further consolidated its leadership in new technologies and digital transformation, investing in new skills and extending its geographical presence.

In particular, Reply has worked alongside key customers with projects aimed not only at helping them overcome the crisis more quickly, but also at seizing new business opportunities brought by a much more digital, connected and automated world. The paths of evolution are numerous and touch all sectors. For example, artificial intelligence, robotics and the Internet of Things are revolutionizing not only products, but also the way they are conceived, manufactured and sold, significantly changing factories, production processes and entire value chains.

Sustainability is impacting all sectors: a concept that today is still often abstract, but has become increasingly predominant in the choices of companies. As Reply we feel this responsibility towards future generations and, although belonging to a sector with low environmental impact, our commitment is total, both in working to minimize our emissions in the future, and in defining a series of consulting and technological services able to support companies in a process of transition to net-zero.

Finally, the first months of 2022 were characterized by a sudden acceleration of the crisis on eastern European borders, resulting in a war that is putting a strain on the economy, civil society and the very stability of economic systems. In this regard, it should be noted that the organizational structure (including the ecosystem of suppliers), the financial solidity of the Group, the diversification of the business in various countries, markets and industrial sectors, has allowed, to date, to absorb all the indirect effects, thanks to the implementation of local actions aimed at minimizing the impacts on operating activities.

Outlook on operations

The future scenario is still uncertain: if the health emergency appears at the moment under control in the countries where we are present, the recent outbreak of the war on the eastern borders of Europe is increasing a situation of tension on all the main markets with medium and long-term consequences that are difficult to anticipate. In any case, the process of transformation towards a new digital economy, which began in 2020, is now unstoppable and opens up ample opportunities for growth and development for companies like Reply. High-speed communication software infrastructures, e-commerce, new digital experiences and a strong acceleration towards automation and green tech continue to represent the founding elements of the economy in the coming years.

Motion for the approval of the financial statement and allocation of the result for the financial year

The financial statements at year end 2021 of Reply S.p.A. prepared in accordance with International Financial Reporting Standards (IFRS), recorded a net income amounting to 111,243,694 Euros and net shareholders’ equity on 31 December 2021 amounted to 551,042,871 Euros thus formed:

The Board of Directors in submitting to the Shareholders the approval of the financial statements (Separate Statements) as at 31 December 2021 showing a net result of 111,243,694 Euros, proposes that the shareholders resolve:

to approve the financial statement (Separate Statements) of Reply S.p.A. which records net profit for the financial year of 111,243,694 Euros;

to approve the motion to allocate the net result of 111,243,694 as follows:

a unit dividend to shareholders amounting to 0,80 Euros for each ordinary share with a right, therefore excluding treasury shares, with payment date fixed on 25 May 2022, coupon cut-off date 23 May 2022 and record date, determined in accordance with Article 83-terdecies of Legislative Decree no. 58/1998 set on 24 May 2022;

having the Legal reserve reached the limit of one fifth of the share capital pursuant to article 2430 of the Italian Civil Code, the residual amount to be allocated to the Retained earnings reserve;

to approve, pursuant to Article 22 of the Articles of association, the proposal of the Remuneration Committee to distribute to Directors entrusted with operational powers, a shareholding of the profits of the Parent Company, to be established in the amount of 3,783,000.00 Euros.

Turin, 15 March 2022

/f/ Mario Rizzante

For the Board of Directors

The Chairman

Mario Rizzante