Income Statement (*)

Statement of comprehensive income

Statement of financial position (*)

Statement of changes in equity

Statement of cash flows

Notes to the financial statements

NOTE 1 - GENERAL INFORMATION

Reply [MTA, STAR: REY] is specialized in the implementation of solutions based on new communication and digital media. Reply, consisting of a network of specialized companies, assists important European industries belonging to Telco & Media, Manufacturing & Retail, Bank & Insurances and Public Administration sectors, in defining and developing new business models utilizing Big Data, Cloud Computing, CRM, Mobile, Social Media and Internet of Things paradigms. Reply’s services include: consulting, system integration, application management and Business Process Outsourcing. (www.reply.com)

The company mainly carries out the operational coordination and technical management of the group and also the administration, financial assistance and some purchase and marketing activities. Reply also manages business relations for some of its main clients.

NOTE 2 - ACCOUNTING PRINCIPLES AND BASIS OF CONSOLIDATION

COMPLIANCE WITH INTERNATIONAL ACCOUNTING PRINCIPLES

The 2017 Financial Statements have been prepared in accordance with International Financial Reporting Standards (“IFRS”) issued by the International Accounting Standards Board (“IASB”) and endorsed by the European Union, and with the provisions implementing Article 9 of Legislative Decree No. 38/2005.

The designation “IFRS” also includes all valid International Accounting Standards (“IAS”), as well as all interpretations of the International Financial Reporting Interpretations Committee (“IFRIC”), formerly the Standing Interpretations Committee (“SIC”).

In compliance with European Regulation No. 1606 of 19 July 2002, beginning in 2005, the Reply Group adopted the International Financial Reporting Standards (“IFRS”) for the preparation of its Consolidated Financial Statements. On the basis of national legislation implementing the aforementioned Regulation, those accounting standards were also used to prepare the separate Financial Statements of the Parent Company, Reply S.p.A., for the first time for the year ended 31 December 2006.

It is hereby specified that the accounting standards applied conform to those adopted for the preparation of the initial Statement of Assets and Liabilities as at 1 January 2005 according to the IFRS, as well as for the 2005 Income Statement and the Statement of Assets and Liabilities as at 31 December 2005, as re-presented according to the IFRS and published in the special section of these Financial Statements.

GENERAL PRINCIPLES

The Financial Statements were prepared under the historical cost convention, modified as required for the measurement of certain financial instruments. The criterion of fair value was adopted as defined by IAS 39.

The Financial Statements have been prepared on the going concern assumption. In this respect, despite operating in a difficult economic and financial environment, the Company’s assessment is that no material uncertainties (as defined in paragraph 25 of IAS 1) exist relative to its ability to continue as a going concern.

These Financial Statements are expressed in Euros and are compared to the Financial Statements of the previous year prepared in accordance with the same principles.

These Financial Statements have been drawn up under the general principles of continuity, accrual based accounting, coherent presentation, relevancy and aggregation, prohibition of compensation and comparability of information.

The fiscal year consists of a twelve (12) month period and closes on the 31 December each year.

FINANCIAL STATEMENTS

The Financial Statements include statement of income, statement of comprehensive income, statement of financial position, statement of changes in shareholders’ equity, statement of cash flows and the explanatory notes.

The income statement format adopted by the company classifies costs according to their nature, which is deemed to properly represent the company’s business.

The Statement of financial position is prepared according to the distinction between current and non-current assets and liabilities. The statement of cash flows is presented using the indirect method. The most significant items are disclosed in a specific note in which details related to the composition and changes compared to the previous year are provided.

It is further noted that, to comply with the indications provided by Consob Resolution No. 15519 of 27 July 2006 “Provisions as to the format of Financial Statements”, in addition to mandatory tables, specific supplementary Income Statement and Balance Sheet formats have been added that report significant amounts of positions or transactions with related parties indicated separately from their respective items of reference.

TANGIBLE ASSETS

Tangible fixed assets are stated at cost, net of accumulated depreciation and impairment losses.

Goods made up of components, of significant value, that have different useful lives are considered separately when determining depreciation.

In compliance with IAS 36 – Impairment of assets, the carrying value is immediately remeasured to the recoverable value, if lower.

Depreciation is charged so as to write off the cost or valuation of assets, over their estimated useful lives, using the straight-line method, on the following bases:

Ordinary maintenance costs are fully expensed as incurred. Incremental maintenance costs are allocated to the asset to which they refer and depreciated over their residual useful lives.

Improvement expenditures on rented property are allocated to the related assets and depreciated over the shorter between the duration of the rent contract or the residual useful lives of the relevant assets.

The gain or loss arising on the disposal or retirement of an asset is determined as the difference between the sales proceeds and the carrying amount of the asset and is recognized in income.

GOODWILL

Goodwill is an intangible asset with an indefinite life, deriving from business combinations recognized using the purchase method, and is recorded to reflect the positive difference between purchase cost and the Company’s interest at the time of acquisition of the fair value of the assets, liabilities and identifiable contingent liabilities attributable to the subsidiary.

Goodwill is not amortized, but is tested for impairment annually or more frequently if specific events or changes in circumstances indicate that it might be impaired. After initial recognition, goodwill is measured at cost less any accumulated impairment losses.

Impairment losses are recognized immediately as expenses that cannot be recovered in the future.

Goodwill deriving from acquisitions made prior to the transition date to IFRS are maintained at amounts recognized under Italian GAAP at the time of application of such standards and are subject to impairment tests at such date.

OTHER INTANGIBLE ASSETS

Intangible fixed assets are those lacking an identifiable physical aspect, are controlled by the company and are capable of generating future economic benefits.

Other purchased and internally-generated intangible assets are recognized as assets in accordance with IAS 38 – Intangible Assets, where it is probable that the use of the asset will generate future economic benefits and where the costs of the asset can be determined reliably.

Such assets are measured at purchase or manufacturing cost and amortized on a straight-line basis over their estimated useful lives, if these assets have finite useful lives.

Other intangible assets acquired as part of an acquisition of a business are capitalized separately from goodwill if their fair value can be measured reliably.

In case of intangible fixed assets purchased for which availability for use and relevant payments are deferred beyond normal terms, the purchase value and the relevant liabilities are discounted by recording the implicit financial charges in their original price.

Expenditure on research activities is recognized as an expense in the period in which it is incurred.

Development costs can be capitalized on condition that they can be measured reliably and that evidence is provided that the asset will generate future economic benefits.

An internally-generated intangible asset arising from the company’s e-business development (such as informatics solutions) is recognized only if all of the following conditions are met:

-

An asset is created that can be identified (such as software and new processes);

-

It is probable that the asset created will generate future economic benefits;

-

The development cost of the asset can be measured reliably.

These assets are amortized when launched or when available for use. Until then, and on condition that the above terms are respected, such assets are recognized as construction in progress. Amortization is determined on a straight line basis over the relevant useful lives.

When an internally-generated intangible asset cannot be recorded at balance sheet, development costs are recognized to the statement of income in the period in which they are incurred.

INTANGIBLE ASSETS WITH INDEFINITE USEFUL LIFE

Intangible assets with indefinite useful lives consist principally of acquired trademarks which have no legal, contractual, competitive, economic, or other factors that limit their useful lives. Intangible assets with indefinite useful lives are not amortized, as provided by IAS 36, but are tested for impairment annually or more frequently whenever there is an indication that the asset may be impaired. Any impairment losses are not subject to subsequent reversals.

IMPAIRMENT

At each balance sheet date, the Company reviews the carrying amounts of its tangible and intangible assets to determine whether there is any indication that those assets have suffered an impairment loss. If any such indication exists, the recoverable amount of the asset is estimated in order to determine the extent of the impairment loss (if any). Where it is not possible to estimate the recoverable amount of an individual asset, the Company estimates the recoverable amount of the cash-generating unit to which the asset belongs.

An intangible asset with an indefinite useful life is tested for impairment annually or more frequently, whenever there is an indication that the asset may be impaired.

The recoverable amount of an asset is the higher of fair value less disposal costs and its value in use. In assessing its value in use, the pre-tax estimated future cash flows are discounted to their present value using a pre-tax discount rate that reflects current market assessments of the time value of money and the risks specific to the asset. Its value in use is determined net of tax in that this method produces values largely equivalent to those obtained by discounting cash flows net of tax at a pre-tax discount rate derived, through an iteration, from the result of the post-tax assessment. The assessment is carried out for the individual asset or for the smallest identifiable group of cash generating assets deriving from ongoing use, (the so-called Cash generating unit). With reference to goodwill, Management assesses return on investment with reference to the smallest cash generating unit including goodwill.

If the recoverable amount of an asset (or cash-generating unit) is estimated to be less than its carrying amount, the carrying amount of the asset is reduced to its recoverable amount. Impairment losses are recognized as an expense immediately. When the recognition value of the Cash generating unit, inclusive of goodwill, is higher than the recoverable value, the difference is subject to impairment and attributable firstly to goodwill; any exceeding difference is attributed on a pro-quota basis to the assets of the Cash generating unit.

Where an impairment loss subsequently reverses, the carrying amount of the asset, (or cash-generating unit), with the exception of goodwill, is increased to the revised estimate of its recoverable amount, but so that the increased carrying amount that would have been determined had no impairment loss been recognized for the asset. A reversal of an impairment loss is recognized as income immediately, unless the relevant asset is carried at a revalued amount, in which case the reversal of the impairment loss is treated as a revaluation increase.

EQUITY INVESTMENTS

Investments in subsidiaries and associated companies are valued using the cost method. As implementation of such method, they are subject to an impairment test if there is any objective evidence that these investments have been impaired, due to one or more events that occurred after the initial measurement if such events have had an impact on future cash flows, thus inhibiting the distribution of dividends. Such evidence exists when the subsidiary’s and associate’s operating margins are repetitively and significantly negative. If such is the case, impairment is recognized as the difference between the carrying value and the recoverable value, normally determined on the basis of fair value less disposal costs, normally determined through the application of the market multiples to prospective EBIT or to the value in use.

At each reporting period, the Company assesses whether there is objective evidence that a write-down due to impairment of an equity investment recognized in previous periods may be reduced or derecognized. Such evidence exists when the subsidiary’s and associate’s operating margins are repetitively and significantly positive. In this case, the recoverable value is re-measured and eventually the investment is restated at initial cost.

Equity investments in other companies, comprising non current financial assets not held for trading, are measured at fair value, if it can be determined. Any subsequent gains and losses resulting from changes in fair value are recognized directly in Shareholders’ equity until the investment is sold or impaired; the total recognized in equity up to that date are recognized in the Income Statement for the period.

Minor investments in other companies for which fair value is not available are measured at cost, and adjusted for any impairment losses.

Dividends are recognized as financial income from investments when the right to collect them is established, which generally coincides with the shareholders’ resolution. If such dividends arise from the distribution of reserves prior to the acquisition, these dividends reduce the initial acquisition cost.

CURRENT AND NON CURRENT FINANCIAL ASSETS

Financial assets are recognized on the Company’s balance sheet when the Company becomes a party to the contractual provisions of the instrument.

Investments are recognized and written-off the balance sheet on a trade-date basis and are initially measured at cost, including transaction costs.

At subsequent reporting dates, financial assets that the Company has the expressed intention and ability to hold to maturity (held-to-maturity securities) are measured at amortized cost according to the effective interest rate method, less any impairment loss recognized to reflect irrecoverable amounts, and are classified among non current financial assets.

Investments other than held-to maturity securities are classified as either held-for-trading or available-for-sale, and are measured at subsequent reporting dates at fair value. Where financial assets are held for trading purposes, gains and losses arising from changes in fair value are included in the net profit or loss for the period. For available-for-sale investments, gains and losses arising from changes in fair value are recognized directly in equity, until the security is disposed of or is determined to be impaired, at which time the cumulative gain or loss previously recognized in equity is included in the net profit or loss for the period. This item is stated in the current financial assets.

TRANSFER OF FINANCIAL ASSETS

The Company derecognizes financial assets from its Financial Statements when, and only when, the contractual rights to the cash flows deriving from the assets expire or the Company transfers the financial asset. In the case of transfer of the financial asset:

-

If the entity substantially transfers all of the risks and benefits of ownership associated with the financial asset, the Company derecognizes the financial asset from the Financial Statements and recognizes separately as assets or liabilities any rights or obligations originated or maintained through the transfer;

-

If the Company maintains substantially all of the risks and benefits of ownership associated with the financial assets, it continues to recognize it;

-

If the Company does not transfer or maintain substantially all of the risks and benefits of ownership associated with the financial asset, it determines whether or not it has maintained control of the financial asset. In this case:

-

If the Company has not maintained control, it derecognizes the financial asset from its Financial Statements and recognizes separately as assets or liabilities any rights or obligations originated or maintained through the transfer;

-

If the Company has maintained control, it continues to recognize the financial asset to the extent of its residual involvement with such financial asset.

At the time of removal of financial assets from the balance sheet, the difference between the carrying value of assets and the fees received or receivable for the transfer of the asset is recognized in the income statement.

Trade payables and receivables and other current assets and liabilities

Trade payables and receivables and other current assets and liabilities are measured at nominal value and eventually written down to reflect their recoverable amount.

Write-downs are determined to the extent of the difference of the carrying value of the receivables and the present value of the estimated future cash flows.

Receivables and payables denominated in non EMU currencies are stated at the exchange rate at period end provided by the European Central Bank.

Cash and cash equivalents

The item cash and cash equivalents includes cash, banks and reimbursable deposits on demand and other short term financial investments readily convertible in cash and are not subject to significant risks in terms of change in value.

Treasury shares

Treasury shares are presented as a deduction from equity. All gains and losses from the sale of treasury shares are recorded in a special Shareholders’ equity reserve.

Financial liabilities and equity investments

Financial liabilities and equity instruments issued by the Company are presented according to their substance arising from their contractual obligations and in accordance with the definitions of financial liabilities and equity instruments. The latter are defined as those contractual obligations that give the right to benefit in the residual interests of the Company’s assets after having deducted its liabilities.

The accounting standards adopted for specific financial liabilities or equity instruments are outlined below:

-

Bank borrowings

Interest-bearing bank loans and overdrafts are recorded at the proceeds received, net of direct issue costs and subsequently stated at its amortized cost, using the prevailing market interest rate method.

-

Equity instruments

Equity instruments issued by the Group are stated at the proceeds received, net of direct issuance costs.

-

Non current financial liabilities

Liabilities are stated according to the amortization cost.

DERIVATIVE FINANCIAL INSTRUMENTS AND OTHER HEDGING TRANSACTIONS

The Company’s activities are primarily subject to financial risks associated with fluctuations in interest rates. Such interest rate risks arise from bank borrowings. In order to hedge such risks, the Company’s policy consists of converting fluctuating rate liabilities in constant rate liabilities and treating them as cash flow hedges. The use of such instruments is disciplined by written procedures in line with the Company risk strategies that do not contemplate derivative financial instruments for trading purposes.

In accordance with IAS 39, derivative financial instruments qualify for hedge accounting only when at the inception of the hedge there is formal designation and sufficient documentation that the hedge is highly effective and that its effectiveness can be reliably measured. The hedge must be highly effective throughout the different financial reporting periods for which it was designated.

All derivative financial instruments are measured in accordance with IAS 39 at fair value.

Changes in the fair value of derivative financial instruments that are designated and effective as hedges of future cash flows relating to Company commitments and forecasted transactions are recognized directly in Shareholder’s equity, while the ineffective portion is immediately recorded in the Income Statement.

If the hedged company commitment or forecasted transaction results in the recognition of an asset or liability, then, at the time the asset or liability is recognized, associated gains or losses on the derivative that had previously been recognized in equity are included in the initial measurement of the asset or liability.

For hedges that do not result in the recognition of an asset or a liability, amounts deferred in equity are recognized in the income statement in the same period in which the hedge commitment or forecasted transaction affects net profit or loss, for example, when the future sale actually occurs.

For effective hedging against a change in fair value, the hedged item is adjusted by the changes in fair value attributable to the risk hedged with a balancing entry in the Income Statement. Gains and losses arising from the measurement of the derivative are also recognized at the income statement.

Changes in the fair value of derivative financial instruments that no longer qualify as hedge accounting are recognized in the Income Statement of the period in which they arise.

Hedge accounting is discontinued when the hedging instrument expires or is sold, terminated, or exercised or no longer qualifies for hedge accounting. At that time, any cumulative gain or loss on the hedging instrument recognized in equity is retained in equity until the forecasted transaction is no longer expected to occur; the net cumulative gain or loss recognized in equity is transferred to the net profit or loss for the period.

Embedded derivatives included in other financial instruments or in other contractual obligations are treated as separate derivatives, when their risks and characteristics are not closely related to those of the financial instrument that houses them and the latter are not measured at fair value with recognition of the relative gains and losses in the Income Statement.

EMPLOYEE BENEFITS

The scheme underlying the employee severance indemnity of the Italian Group companies (the TFR) was classified as a defined benefit plan up until 31 December 2006. The legislation regarding this scheme was amended by Law No. 296 of 27 December 2006 (the “2007 Finance Law”) and subsequent decrees and regulations issued in the first part of 2007. In view of these changes, and with specific reference to those regarding companies with at least 50 employees, this scheme only continues to be classified as a defined benefit plan in the Financial Statements for those benefits accruing up to 31 December 2006 (and not yet settled by the balance sheet date), while after that date the scheme is classified as a defined contribution plan.

Employee termination indemnities (“TFR”) are classified as a “post-employment benefit”, falling under the category of a “defined benefit plan”; the amount already accrued must be projected in order to estimate the payable amount at the time of employee termination and subsequently be discounted through the “projected unit credit method”, an actuarial method based on demographic and finance data that allows the reasonable estimate of the extent of benefits that each employee has matured in relation to the time worked. Through actuarial measurement, interest cost is recognized as financial gains or losses and represents the figurative expenditure that the Company would bear by securing a market loan for an amount corresponding to the Employee Termination Indemnities (“TFR”).

Actuarial income and losses that reflect the effects resulting from changes in the actuarial assumptions used are directly recognized in Shareholders’ equity.

SHARE-BASED PAYMENT PLANS

The Company has applied the standard set out by IFRS 2 “Share-based payment”.

Share-based payments are measured at fair value at granting date. Such amount is recognized in the Income Statement, with a balancing entry in Shareholders’ equity, on a straight-line basis and over the (vesting period). The fair value of the option, measured at the granting date, is assessed through actuarial calculations, taking into account the terms and conditions of the options granted.

The stock options resolved in the previous financial years have been exercised and therefore the Company does not have existing stock option plans.

PROVISIONS AND RESERVES FOR RISKS

Provisions for risks and liabilities are costs and liabilities having an established nature and the existence of which is certain or probable that at the reporting date the amount cannot be determined or the occurrence of which is uncertain. Such provisions are recognized when a commitment actually exists arising from past events of legal or contractual nature or arising from statements or company conduct that determine valid expectations from the persons involved (implicit obligations).

Provisions are recognized when the Company has a present commitment arising from a past event and it is probable that it will be required to fulfil the commitment. Provisions are accrued at the best estimate of the expenditure required to settle the liability at the balance sheet date, and are discounted when the effect is significant.

REVENUE RECOGNITION

Revenue is recognized if it is probable that the economic benefits associated with the transaction will flow to the Company and the revenue can be measured reliably.

Revenue from sales and services is recognized when the transfer of all the risks and benefits arising from the passage of title takes place or upon execution of a service.

Revenues from services include the activities the Company carries out directly with respect to some of its major clients in relation to their businesses. These activities are also carried out in exchange for services provided by other Group companies, and the costs for such services are recognized as Services and other costs.

Revenues from sales of products are recognized when the risks and rewards of ownership of goods are transferred to the customer. Revenues are recorded net of discounts, allowances, settlement discounts and rebates and charged against profit for the period in which the corresponding sales are recognized.

Interest income is accrued on a time basis, by reference to the principal outstanding and at the effective interest rate applicable that represents the discounted interest rate of the future estimated proceeds estimated over the expected life of the financial asset in order to bring them to the accounting value of the same asset.

Dividends from investments is recognized when the shareholders’ rights to receive payment has been established.

FINANCIAL INCOME AND EXPENSES

Financial income and expenses are recognized and measured in the income statement on an accrual basis.

TAXATION

Income tax represents the sum of the tax currently payable and deferred tax. The tax currently payable is based on taxable profit for the year. Taxable profit defers from the profit as reported in the income statement because it excludes items of income or expense that are taxable or deductible in other years and it further excludes items that are never taxable or deductible.

Current income tax is entered for each individual company based on an estimate of taxable income in compliance with existing legislation and tax rates or as substantially approved at the period closing date in each country, considering applicable exemptions and tax credit.

Deferred tax is the tax expected to be payable or recoverable on differences between the carrying amount of assets and liabilities in the Financial Statements and the corresponding tax basis used in the computation of taxable profit, and is accounted for using the balance sheet liability method. Deferred tax liabilities are generally recognized for all taxable temporary differences and tax assets are recognized to the extent that it is probable that taxable profits will be available against which deductible temporary differences can be utilized. Such assets and liabilities are not recognized if the temporary difference arises from goodwill or from the initial recognition (other than in a business combination) of other assets and liabilities in a transaction that affects neither the tax profit nor the accounting profit.

Deferred tax liabilities are recognized for taxable temporary differences arising on investments in subsidiaries and associates and interests arising in joint ventures, except where the Company is able to control the reversal of the temporary difference and it is probable that the temporary difference will not reverse in the foreseeable future.

The carrying amount of deferred tax assets is reviewed at each balance sheet date and reduced to the extent that it is no longer probable that sufficient taxable profit will be available to allow all or part of the asset to be recovered.

Deferred tax is calculated at the tax rates that are expected to apply to the period when the liability is settled or the asset realized. Deferred tax is charged or credited in the income statement, except when it relates to items charged or credited directly to equity, in which case the deferred tax is also dealt with in equity.

Deferred tax assets and liabilities are offset when they relate to income taxes levied by the same taxation authority and the Company intends to settle its current tax assets and liabilities on a net basis.

In the event of changes to the accounting value of deferred tax assets and liabilities deriving from a change in the applicable tax rates and relevant legislation, the resulting deferred tax amount is entered in income statement, unless it refers to debited or credited amounts previously recognized to Shareholders’ equity.

EARNINGS PER SHARE

Basic earnings per share is calculated with reference to the profit for the period of the Company and the weighted average number of shares outstanding during the year. Treasury shares are excluded from this calculation.

Diluted earnings per share is determined by adjusting the basic earnings per share to take account of the theoretical conversion of all potential shares, being all financial instruments that are potentially convertible into ordinary shares, with diluting effect.

USE OF ESTIMATIONS

The preparation of the Financial Statements and relative notes under IFRS requires that management makes estimates and assumptions that have effect on the measurement of assets and liabilities and on disclosures related to contingent assets and liabilities at the reporting date. The actual results could differ from such estimates. Estimates are used to accrue provisions for risks on receivables, to measure development costs, to measure contract work in progress, employee benefits, income taxes and other provisions. The estimations and assumptions are reviewed periodically and the effects of any changes are recognized immediately in income.

Changes in estimations and reclassifications

There were no changes of estimates or reclassifications during the 2017 reporting period.

NEW STANDARDS, INTERPRETATIONS AND AMENDMENTS ADOPTED BY THE COMPANY FROM 1 JANUARY 2017

Reply S.p.A. applied for the first time certain amendments to the standards, which are effective for annual periods beginning on or after 1 January 2017. Reply S.p.A. has not early adopted any standards, interpretations or amendments that have been issued but are not yet effective.

The nature and the impact of each amendment is described below:

Amendments to IAS 7 Statement of Cash Flows: Disclosure Initiative

The amendments require entities to provide disclosure of changes in their liabilities arising from financing activities, including both changes arising from cash flows and non-cash changes (such as foreign exchange gains or losses). Reply S.p.A. has provided the information in Note 28.

Amendments to IAS 12 Income Taxes: Recognition of Deferred Tax Assets for Unrealized Losses

The amendments clarify that an entity needs to consider whether tax law restricts the sources of taxable profits against which it may make deductions on the reversal of deductible temporary difference related to unrealized losses. Furthermore, the amendments provide guidance on how an entity should determine future taxable profits and explain the circumstances in which taxable profit may include the recovery of some assets for more than their carrying amount.

The Company applied amendments retrospectively. However, their application has no effect on the Company’s financial position and performance as the Company has no deductible temporary differences or assets that are in the scope of the amendments.

STANDARDS ISSUED BUT NOT YET EFFECTIVE

The standards and interpretations that are issued, but not yet effective, up to the date of issuance of the Company’s financial statements are disclosed below. The Company intends to adopt these standards, if applicable, when they become effective.

IFRS 9 Financial Instruments

In July 2014, the IASB issued the final version of IFRS 9 Financial Instruments, which replaces IAS 39 Financial Instruments: Recognition and Measurement and all previous versions of IFRS 9. IFRS 9 brings together all three aspects of the accounting for financial instruments project: classification and measurement, impairment and hedge accounting. IFRS 9 is effective for annual periods beginning on or after 1 January 2018, with early application permitted. Except for hedge accounting, retrospective application is required but providing comparative information is not compulsory. For hedge accounting, the requirements are generally applied prospectively, with some limited exceptions.

The Company plans to adopt the new standard on the required effective date and will not restate comparative information. During 2017, the Company has performed a detailed impact assessment of all three aspects of IFRS 9. This assessment is based on currently available information and may be subject to changes arising from further reasonable and supportable information being made available to the Company in 2018 when the Company will adopt IFRS 9. Overall, the Company expects no significant impact on its statement of financial position and equity.

-

Classification and measurement

The Company does not expect a significant impact on its balance sheet or equity on applying the classification and measurement requirements of IFRS 9. It expects to continue measuring at fair value all financial assets currently held at fair value.

Loans as well as trade receivables are held to collect contractual cash flows and are expected to give rise to cash flows representing solely payments of principal and interest. The Company analyzed the contractual cash flow characteristics of those instruments and concluded that they meet the criteria for amortized cost measurement under IFRS 9. Therefore, reclassification for these instruments is not required.

-

Impairment

IFRS 9 requires the Company to record expected credit losses on all of its debt securities, loans and trade receivables, either on a 12-month or lifetime basis. The Company will apply the simplified approach and record lifetime expected losses on all trade receivables. According to the performed assessment, the Company does not expect a significant impact on its loss allowance.

-

Hedge accounting

The Company determined that all existing hedge relationships that are currently designated in effective hedging relationships will continue to qualify for hedge accounting under IFRS 9. The Company has chosen not to retrospectively apply IFRS 9 on transition to the hedges where the Company excluded the forward points from the hedge designation under IAS 39. As IFRS 9 does not change the general principles of how an entity accounts for effective hedges, applying the hedging requirements of IFRS 9 will not have a significant impact on Company’s financial statements.

IFRS 15 Revenue from Contracts with Customers

IFRS 15 was issued in May 2014, and amended in April 2016, and will supersede all current revenue recognition requirements under IFRS. Either a full retrospective application or a modified retrospective application is required for annual periods beginning on or after 1 January 2018. Early adoption is permitted.

The standard requires a company to recognize revenue upon transfer of control of goods or services to a customer at an amount that reflects the consideration it expects to receive in exchange for transferring goods or services to a customer, using a five-step process.

The new standard also requires additional disclosures about the nature, amount, timing and uncertainty of revenue and cash flows arising from customer contracts.

The Company plans to adopt the new standard on the required effective date using the full retrospective method. During 2016, the Company performed a preliminary assessment of IFRS 15, which was continued with a more detailed analysis completed in 2017. On the basis of this assessment, the Company’s revenues will continue to be recognized in a manner consistent with accounting guidance in prior years. It is not foreseen an impact on equity and to the Company’s Net profit.

Amendments to IFRS 10 and IAS 28: Sale or Contribution of Assets between an Investor and its Associate or Joint Venture

The amendments address the conflict between IFRS 10 and IAS 28 in dealing with the loss of control of a subsidiary that is sold or contributed to an associate or joint venture. The amendments clarify that the gain or loss resulting from the sale or contribution of assets that constitute a business, as defined in IFRS 3, between an investor and its associate or joint venture, is recognized in full. Any gain or loss resulting from the sale or contribution of assets that do not constitute a business, however, is recognized only to the extent of unrelated investors’ interests in the associate or joint venture. The IASB has deferred the effective date of these amendments indefinitely, but an entity that early adopts the amendments must apply them prospectively.

IFRS 2 Classification and Measurement of Share-based Payment Transactions — Amendments to IFRS 2

The IASB issued amendments to IFRS 2 Share-based Payment that address three main areas: the effects of vesting conditions on the measurement of a cash-settled share-based payment transaction; the classification of a share-based payment transaction with net settlement features for withholding tax obligations; and accounting where a modification to the terms and conditions of a share-based payment transaction changes its classification from cash settled to equity settled.

On adoption, entities are required to apply the amendments without restating prior periods, but retrospective application is permitted if elected for all three amendments and other criteria are met.

The amendments are effective for annual periods beginning on or after 1 January 2018, with early application permitted. The Company does not expect impact from the applying of those amendments.

IFRS 16 Leases

IFRS 16 was issued in January 2016 and it replaces IAS 17 Leases, IFRIC 4 Determining whether an Arrangement contains a Lease, SIC-15 Operating Leases-Incentives and SIC-27 Evaluating the Substance of Transactions Involving the Legal Form of a Lease. IFRS 16 sets out the principles for the recognition, measurement, presentation and disclosure of leases and requires lessees to account for all leases under a single on-balance sheet model similar to the accounting for finance leases under IAS 17. The standard includes two recognition exemptions for lessees – leases of ’low-value’ assets (e.g., personal computers) and short-term leases (i.e., leases with a lease term of 12 months or less). At the commencement date of a lease, a lessee will recognize a liability to make lease payments (i.e., the lease liability) and an asset representing the right to use the underlying asset during the lease term (i.e., the right-of-use asset). Lessees will be required to separately recognize the interest expense on the lease liability and the depreciation expense on the right-of-use asset.

Lessees will be also required to remeasure the lease liability upon the occurrence of certain events (e.g., a change in the lease term, a change in future lease payments resulting from a change in an index or rate used to determine those payments). The lessee will generally recognize the amount of the remeasurement of the lease liability as an adjustment to the right-of-use asset.

Lessor accounting under IFRS 16 is substantially unchanged from today’s accounting under IAS 17. Lessors will continue to classify all leases using the same classification principle as in IAS 17 and distinguish between two types of leases: operating and finance leases.

IFRS 16 also requires lessees and lessors to make more extensive disclosures than under IAS 17.

IFRS 16 is effective for annual periods beginning on or after 1 January 2019. Early application is permitted, but not before an entity applies IFRS 15. A lessee can choose to apply the standard using either a full retrospective or a modified retrospective approach. The standard’s transition provisions permit certain reliefs.

In 2018, the Company will continue to assess the potential effect of IFRS 16 on its consolidated financial statements.

NOTE 3 - Risk management

Reply S.p.A. operates at a world-wide level and for this reason its activities are exposed to various types of financial risks: market risk (broken down in exchange risk, interest rate risk on financial flows and on “fair value”, price risk), credit risk and liquidity risk.

To minimize risks Reply utilizes derivative financial instruments. At a central level it manages the hedging of principle operations. Reply S.p.A. does not detain derivate financial instruments for negotiating purposes.

Credit Risk

For business purposes, specific policies are adopted in order to guarantee that clients honor payments.

With regards to financial counterparty risk, the company does not present significant risk in credit-worthiness or solvency. For newly acquired clients, the Company accurately verifies their capability in terms of facing financial commitments. Transactions of a financial nature are undersigned only with primary financial institutions.

LIQUIDITY RISK

The Company is exposed to funding risk if there is difficulty in obtaining finance for operations at any given point in time.

The cash flows, funding requirements and liquidity of Group companies are monitored and managed on a centralized basis through the Group Treasury. The aim of this centralized system is to optimize the efficiency and effectiveness of the management of the Group’s current and future capital resources (maintaining an adequate level of cash and cash equivalents and the availability of reserves of liquidity that are readily convertible to cash and committed credit).

The difficulties both in the markets and in the financial markets require special attention to the management of liquidity risk, and in that sense particular emphasis is being placed on measures taken to generate financial resources through operations and on maintaining an adequate level of available liquidity. The Company therefore plans to meet its requirements to settle financial liabilities as they fall due and to cover expected capital expenditures by using cash flows from operations and available liquidity, renewing or refinancing bank loans.

RISKS ASSOCIATED WITH FLUCTUATIONS IN CURRENCY AND INTEREST RATES

As the company operates mainly in a “Euros area” the exposure to currency risks is limited.

The exposure to interest rate risk arises from the need to fund operating activities and the necessity to deploy surplus. Changes in market interest rates may have the effect of either increasing or decreasing the company’s net profit/(loss), thereby indirectly affecting the costs and returns of financing and investing transactions.

The exposure to interest rate risk arises from the need to fund operating activities and M&A investments, as well as the necessity to deploy available liquidity. Changes in market interest rates may have the effect of either increasing or decreasing the Company’s net profit/(loss), thereby indirectly affecting the costs and returns of financing and investing transactions.

The interest rate risk to which the Company is exposed derives from bank loans; to mitigate such risks, Reply S.p.A., when useful, uses derivative financial instruments designated as “cash flow hedges”. The use of such instruments is disciplined by written procedures in line with the Company’s risk management strategies that do not contemplate derivative financial instruments for trading purposes.

NOTE 4 - Other information

Exception allowed under paragraph 4 of Article 2423 of the Italian Civil Code

No exceptions allowed under Article 2423, paragraph 4, of the Italian Civil Code were used in drawing up the annexed Financial Statements.

Fiscal consolidation

The Company has decided to enter into the National Fiscal Consolidation pursuant to articles 117/129 of the TUIR.

Reply S.p.A., Parent Company, acts as the consolidating company and determines just one taxable income for the Group companies that adhere to the Fiscal Consolidation, and will benefit from the possibility of compensating taxable income having fiscal losses in just one tax return.

Each company adhering to the Fiscal Consolidation transfers to Reply S.p.A. its entire taxable income, recognizing a liability with respect to the Company corresponding to the payable IRES; The companies that transfer fiscal losses can register a receivable with Reply, corresponding to IRES on the part of the loss off-set at a Group level and remunerated according to the terms established in the consolidation agreement stipulated among the Group companies.

NOTE 5 - Revenue

Revenues amounted to 378,788,753 Euros and are detailed as follows:

Reply manages business relationships on behalf of some of its major clients. Such activities were recorded in the item Revenues from services to third parties which increased by 5,307,368 Euros.

Revenues from Royalties on the “Reply” trademark refer to charges to subsidiaries, corresponding to 3% of the subsidiaries’ turnover with respect to third parties.

Revenues from Intercompany services and Other intercompany charges refer to activities that Reply S.p.A. carries out for the subsidiaries, and more specifically:

-

operational, co-ordination, technical and quality management;

-

administration, personnel and marketing activities;

-

strategic management services.

NOTE 6 - Other income

Other income that as at 31 December 2017 amounted to 10,201,787 Euros (7,999,405 Euros at 31 December 2016) mainly refer to expenses incurred by Reply S.p.A. and recharged to the Group companies, and include expenses for social events, recharged telephone expenses and training courses.

NOTE 7 - Purchases

Detail is as follows:

The items software and hardware licenses for resale refer to the costs incurred for software licenses for resale to third parties carried out for the Group companies.

The item Other mainly includes the purchase of supplies, e-commerce material, stationary and printed materials (143,542 Euros) and fuel (213,718 Euros).

NOTE 8 - Personnel expenses

Personnel costs amounted to 19,821,559 Euros, with a decrease of 354,994 Euros and are detailed in the following table:

Detail of personnel by category is provided below:

The average number of employees in 2017 was 87 (in 2016 89).

NOTE 9 - Services and other costs

Service and other costs comprised the following:

Professional Services from Group companies, which changed during the year by 12,391,881 Euros, relate to revenues from services to third parties.

Reply S.p.A. carries out commercial fronting activities for some of its major clients, whereas delivery is carried out by the operational companies.

Office expenses include services rendered by related parties in connection with service contracts for the use of premises, legal domicile and secretarial services, as well as utility costs.

NOTE 10 - Amortization, depreciation and write-downs

Depreciation of tangible assets was calculated on the basis of technical-economic rates determined in relation to the residual useful lives of the assets, and which amounted in 2017 to an overall cost of 336,687 Euros. Details of depreciation are provided at the notes to tangible assets.

Amortization of intangible assets amounted in 2017 to an overall cost of 636,708 Euros. Details of depreciation are provided at the notes to intangible assets.

NOTE 11 - Other unusual operating income/(expenses)

Other unusual operating expenses amounted to 2,999,737 Euros and refer to the accrual of risk and expense provisions (3,000,000 Euros).

NOTE 12 - Gain/(losses) on equity investments

Detail is a follows:

Dividends include proceeds from dividends received by Reply S.p.A. from subsidiary companies during the year.

Detail is as follows:

Losses on equity investments refer to write-downs and the year-end losses of several subsidiary companies that were prudentially deemed as non-recoverable with respect to the value of the investment.

For further details see Note 19 herein.

NOTE 13 - Financial income/(expenses)

Detail is as follows:

Interest income from subsidiaries refers to the interest yielding cash pooling accounts of the Group companies included in the centralized pooling system.

Interest expenses refer to the interest expenses on the use of credit facilities with Intesa Sanpaolo and Unicredit.

The item Other mainly includes a loss on exchange rate differences amounting to 2,518 thousand Euros and a gain on exchange rate differences amounting to 336 thousand Euros arising from the translation of balance sheet items not recorded in Euros.

NOTE 14 - Income taxes

The details are provided below:

IRES theoretical rate

The following table provides the reconciliation between the IRES theoretical rate and the fiscal theoretical rate:

Temporary differences, net mainly refer to:

-

Deductible differences amounting to 115,111 thousand Euros arising mainly from the non-taxable share of the dividends received in the financial year (102,733 thousand Euros) due to the subsidized taxation (Patent Box) on the Reply trademark;

-

Non-deductible differences amounting to 22,609 thousand Euros owing mainly to write-down/losses of equity investments (13,456 thousand Euros), Directors’ fees to be paid (3,000 thousand Euros), the accrual to of risk and expense provisions (3,000 thousand Euros) and the exchange rate losses related to foreign currency interest-free loans (2,481 thousand Euros).

CALCULATION OF taxable IRAP

Temporary differences, net refer to:

-

Non-deductible differences amounting to 9,130 thousand Euros mainly due to emoluments to Directors (4,784 thousand Euros) and to accruals and write offs not relevant for the purpose of the calculation of taxable IRAP (3,022 thousand Euros);

-

Deductible differences amounting to 8,826 thousand Euros mainly due to the subsidized taxation (Patent Box) on the Reply trademark (8,584 thousand Euros).

NOTE 15 - Earnings per share

Basic earnings and diluted earnings per share as at 31 December 2017 was calculated with reference to the net profit which amounted to 102,067,710 Euros (17,263,478 Euros at 31 December 2016) divided by the weighted average number of shares outstanding as at 31 December 2017, net of treasury shares, which amounted to 37,407,400 (37,407,400 at 31 December 2016).

It is to be noted that the average number of shares for 2016 was redetermined following the Stock split resolved by the Extraordinary Shareholders’ Meeting on September 13, 2017 through the allotment of 4 shares per each ordinary share owned.

NOTE 16 - Tangible assets

Tangible assets as at 31 December 2017 amounted to 477,824 Euros are detailed as follows:

The item Other mainly includes furniture and costs for improvements to leased assets.

Change in Tangible assets during 2017 is summarized below:

During the year under review the Company made investments amounting to 101,148 Euros, which mainly refer to hardware, automobiles and mobile phones.

NOTE 17 - Goodwill

Goodwill as at 31 December 2017 amounted to 86,765 Euros and refers to the value of business branches (consulting activities related to Information Technology and management support acquired in July 2000.

Goodwill recognized is deemed adequately supported in terms of expected financial results and related cash flows.

NOTE 18 - Other intangible assets

Intangible assets as at 31 December 2017 amounted to 2,096,599 Euros (2,118,907 Euros at 31 December 2016) and are detailed as follows:

Change in intangible assets in 2017 is summarized in the table below:

The item Software is related mainly to software licenses purchased and used internally by the company. The increase is related to software licenses purchased and used internally by the company.

The item Trademark expresses the value of the “Reply” trademark granted to the Parent Company Reply S.p.A. (before Reply Europe Sàrl) on 9 June, 2000, in connection to the Company’s share capital increase that was resolved and undersigned by the Parent Company Alister Holding SA. Such amount is not subject to systematic amortization, and the expected future cash flows are deemed adequate.

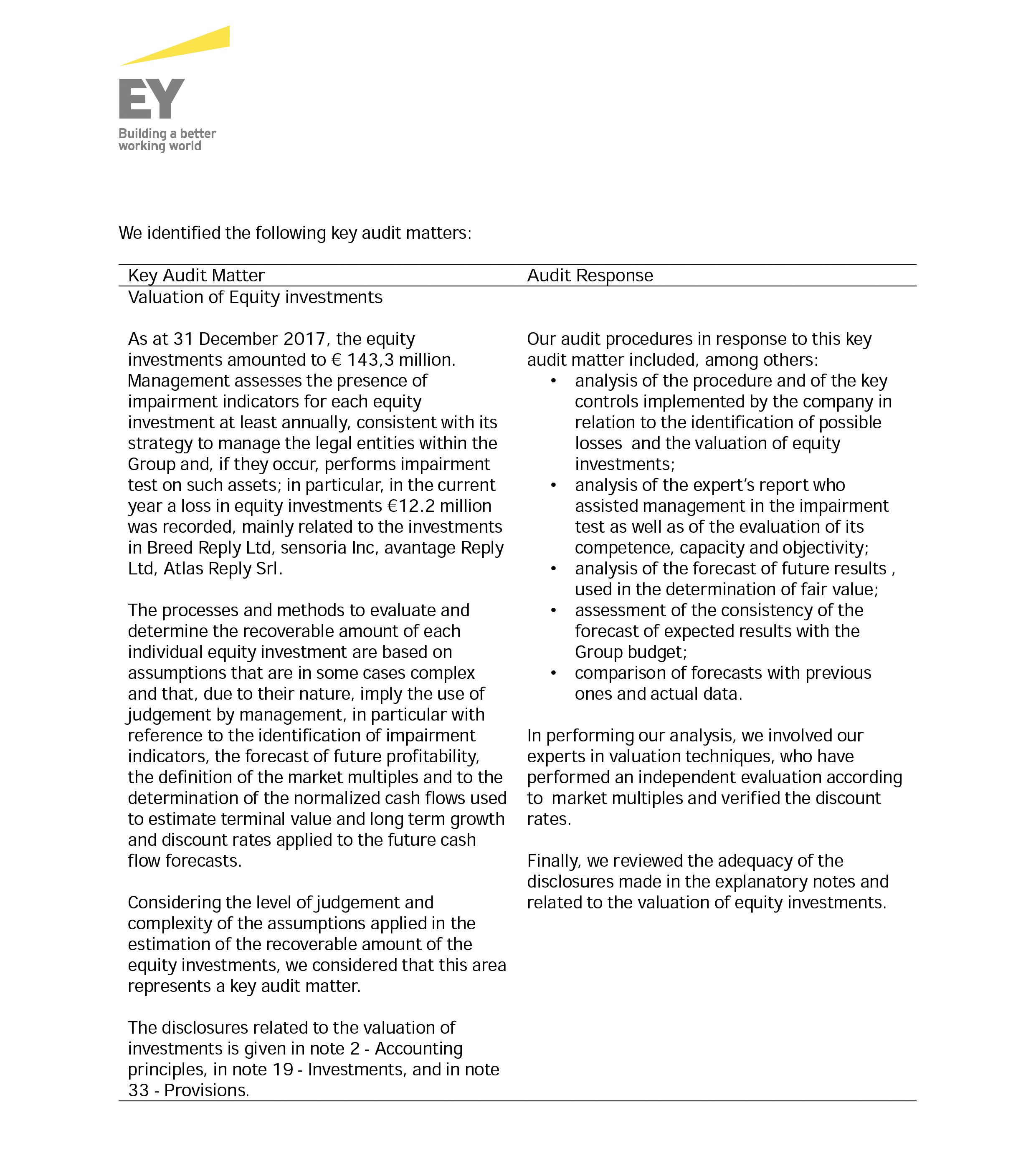

NOTE 19 - Equity investments

The item Equity investments at 31 December 2017 amounted to 143,259,963 Euros, with a decrease of 6,096,232 Euros compared to 31 December 2016.

Acquisitions and subscriptions

Sense Reply S.r.l.

In the month of July 2017 Sense Reply S.r.l. was constituted, a company in which Reply S.p.A. holds 90% of the share capital.

Sprint Reply S.r.l.

In the month of December 2017 Sprint Reply S.r.l. was constituted, a company in which Reply S.p.A. holds 100% of the share capital.

FINANCIAL LOAN REMISSION

The amounts are referred to the waiver of financial loan receivables from some subsidiaries in order to increase their equity position.

WRITE-DOWNS

The amounts recorded reflect losses on some equity investments that are deemed not to be recoverable.

******************

The list of equity investments in accordance with Consob communication no. 6064293 of 28 July 2006 is included in the attachments.

The negative differences arising between the carrying value of the investments and the corresponding portion of their shareholders’ equity are not related to permanent impairment of value, as the carrying value is supported by positive economic and financial forecasts that guarantee the recoverable amount of the investment.

NOTE 20 - Non current financial assets

Detail is as follows:

Guarantee deposits are mainly related to deposits on lease contracts.

Financial receivables from subsidiaries are referred to loans granted to the following companies:

NOTE 21 - Deferred tax assets

This item amounted to 4,634,202 Euros at 31 December 2017 (3,017,480 Euros at 31 December 2016), and included the fiscal charge corresponding to the temporary differences on statutory income and taxable income related to deferred deductible items.

The decision to recognize deferred tax assets is taken by assessing critically whether the conditions exist for the future recoverability of such assets on the basis of expected future results.

There are no deferred tax assets on losses carried forward.

NOTE 22 - Trade receivables

Trade receivables at 31 December 2017 amounted to 372,933,805 Euros and are all collectible within 12 months.

Detail is as follows:

Reply manages business relationships on behalf of some of its major clients. This activity is reflected in the item Third Party Receivables which increased by 14,817,261 Euros.

Receivables from subsidiaries are related to services that the Parent Company Reply S.p.A. carries out in favor of the subsidiary companies at normal market conditions.

Trade receivables are all due within 12 months and do not include significant overdue balances.

In 2017 the provision for doubtful accounts was increased by 22,121 Euros following a specific risk analysis of all the trade receivables, following a utilization of the year amounting to 24,190 Euros.

The carrying amount of Trade receivables in line with its fair value.

NOTE 23 - Other receivables and current assets

Detail is as follows:

The item Tax receivables includes VAT receivables net (6,727,607 Euros) and IRAP and IRES tax prepayments (3,758,729 Euros).

Other receivables from subsidiary companies mainly refer to IRES receivables which are calculated on taxable income, and transferred by the Italian subsidiaries under national fiscal consolidation.

Accrued income and prepaid expenses refer to prepaid expenses arising from the execution of services, lease contracts, insurance contracts and other utility expenses, which are accounted for on an accrual basis.

The carrying value of Other receivables and current assets is deemed to be in line with its fair value.

NOTE 24 - Current financial assets

This item amounted to 82,843,389 Euros (63,168,559 Euros at 31 December 2016) and refers to the total of interest yielding cash pooling accounts of subsidiaries included in the centralized pooling system of the Parent Company Reply S.p.A.; the interest yield on these accounts is in line with current market conditions.

NOTE 25 - Cash and cash equivalents

This item amounted to 63,610,241 Euros, with an increase of 13,501,951 Euros compared to 31 December 2016 and is referred to cash at banks and on hand at year-end.

NOTE 26 - Shareholders’ equity

Share capital

As at 31 December 2017 the fully subscribed paid-in share capital of Reply S.p.A., amounted to 4,863,486 Euros and is made up of no. 37,411,428 ordinary shares having a nominal value of euro 0.13 each.

The Extraordinary Shareholders’ Meeting held on 13 September 2017 resolved to split the 9,352,857 outstanding ordinary shares, with a nominal value of € 0.52 each, into 37,411,428 newly issued ordinary shares, with a nominal value of € 0.13 each, having the same characteristics as outstanding ordinary shares, assigned in the ratio of four new shares in replacement of each existing ordinary share.

Treasury shares

The value of the Treasury shares, amounting to 24,502 Euros, refers to the shares of Reply S.p.A. that at 31 December 2017 were equal to no. 4.028.

Capital reserves

At 31 December 2017 amounted to 79.183.600 Euros, and included the following:

-

Share premium reserve amounting to 23,302,692 Euros.

-

Treasury share reserve amounting to 24,502 Euros, relating to the shares of Reply S.p.A which at 31 December 2017 were equal to no. 4.028.

-

Reserve for the purchase of treasury shares amounting to 49,975,498 Euros.

-

Reserves arising from the merger operation of Reply Deutschland AG. in Reply S.p.A, and include:

-

Share swap surplus reserve amounting to 3,445,485 Euros

-

Surplus annulment reserve amounting to 2,902,479 Euros.

Earnings Reserve

Earning reserves amounted to 208,128,469 Euros and were comprised as follows:

-

The Legal reserve amounting to 972,697 Euros (972,697 Euros at 31 December 2016);

-

Extraordinary reserve amounting to 102,265,360 Euros (95,731,345 Euros at 31 December 2016);

-

Retained earnings amounting to 2,822,701 Euros (2,822,701 Euros at 31 December 2016);

-

Net result totaling 102,067,710 Euros (17,263,478 Euros at 31 December 2016).

Other comprehensive income

Other comprehensive income can be analyzed as follows:

NOTE 27 - Payables to minority shareholders

Payables to Minority shareholders and for Earn-out at 31 December 2017 amounted to 2,364,114 Euros and have not undergone any changes compared to 31 December 2016.

NOTE 28 - FINANCIAL LIABILITIES

Detail is as follows:

The future out payments of the financial liabilities are detailed as follows:

M&A loans refers to credit lines to be used for acquisition operations carried directly by Reply S.p.A. or via companies controlled directly or indirectly by the same.

Following and summarized by main features the ongoing contracts entered into for such a purpose:

Summarized below are the existing contracts entered into for such a purpose:

-

On 25 November 2013 Reply S.p.A entered into a line of credit with Unicredit S.p.A for a total amount amounting to 25,000,000 Euros to be used by 31 December 2015. The loan is reimbursed on a half-year basis deferred to commence on 30 June 2016 and will expire on 31 December 2018. Such credit line was used for 6,053 thousand Euros at 31 December 2017.

-

On 31 March 2015 Reply S.p.A. entered into a line of credit with Intesa Sanpaolo S.p.A. for a total amount of 30,000,000 Euros detailed as follows:

-

Tranche A, amounting to 10,000,000 Euros, entirely used for the reimbursement of the credit line dated 13 November 2013. The loan is reimbursed on a half-year basis deferred to commence on 30 September 2015. Such credit line was used for 5,000 thousand Euros at 31 December 2017.

-

Tranche B, amounting to 20,000,000 Euros, to be used by 30 September 2016.The loan is reimbursed on a half-year basis deferred to commence on 31 March 2017. Such credit line was used for 14,286 thousand Euros at 31 December 2017.

-

On 8 April 2015 Reply S.p.A. entered into a line of credit with Unicredit S.p.A. for a total amount of 10,000,000 Euros entirely used for the reimbursement of the credit line dated 19 September 2012.

-

The loan is reimbursed on a half-year basis deferred to commence on 31 October 2016. Such credit line was used for 2,500 thousand Euros at 31 December 2017.

-

On 30 September 2015 Reply S.p.A. entered into a line of credit with Unicredit S.p.A. for a total amount of 25,000,000 Euros to be used by 30 September 2018. On 17 February 2017 a reduction of the credit line to 1,500,000 was agreed and completely utilized, the loan will be reimbursed on a half year basis deferred to commence on 31 May 2019 and will expire on 30 November 2021. Such credit line was used for 1,500 thousand Euros at 31 December 2017.

-

On 28 July 2016 Reply S.p.A. entered into a line of credit with Intesa San Paolo S.p.A. for a total amount of 49,000 thousand Euros to be used by 30 June 2018. The loan will be reimbursed on a half basis deferred to commence on 30 September 2018 and will expire on 30 September 2021. As at December 31, 2017 this line had not been used.

-

On 21 September 2016 Reply S.p.A. entered onto an Interest Rate Swap contract with Intesa San Paolo S.p.A. with effect from 31 March 2017 and will expire on 31 March 2020.

-

On 17 February 2017 Reply S.p.A. entered into a line of credit with Unicredit S.p.A. for a total amount of 50,000,000 Euros to be used by 28 February 2020. As at December 31, 2017 this line had not been used.

As contractually defined, such ratios are as follows:

At the balance sheet date, Reply fulfilled the Covenants under the various contracts.

The item Other refers to the valuation of derivative hedging instruments. The underlying IRS amounted to 19,286 thousand Euros.

The carrying amount of Financial liabilities is deemed to be in line with its fair value.

Net financial position

In compliance with Consob regulation issued on 28 July 2006 and in accordance with CESR’s “Recommendations for the consistent implementation of the European’s regulation on Prospectuses" issued on 10 February 2005 the Net financial position at 31 December 2017 was as follows:

For further details with regards to the above table see Notes 20, 24 and 25 as well as Note 28.

Change in Financial liabilities during 2017 is summarized below:

NOTE 29 - Employee benefits

The Employee severance indemnity represents the obligation to employees under Italian law (amended by Law no. 296/06) accrued by employees up to 31 December 2006 which will be paid when the employee leaves the company. In certain circumstances, a portion of the accrued liability may be given to an employee during his working life as an advance. This is an unfunded defined benefit plan, under which the benefits are almost fully accrued, with the sole exception of future revaluations.

The procedure for the determination of the Company’s obligation with respect to employees was carried out by an independent actuary according to the following stages:

-

Projection of the Employee severance indemnity already accrued at the assessment date and of the portions that will be accrued until when the work relationship is terminated or when the accrued amounts are partially paid as an advance on the Employee severance indemnities;

-

Discounting, at the valuation date, of the expected cash flows that the company will pay in the future to its own employees;

-

Re-proportioning of the discounted performances based on the seniority accrued at the valuation date with respect to the expected seniority at the time the company must fulfil its obligations.

Reassessment of Employee severance indemnities in accordance with IAS 19 was carried out “ad personam” and on the existing employees, that is analytical calculations were made on each employee in force in the company at the assessment date without considering future work force. The actuarial valuation model is based on the so called technical bases which represent the demographic, economic and financial assumptions underlying the parameters included in the calculation.

The assumptions adopted can be summarized as follows:

In accordance with IAS 19, Employment severance indemnities at 31 December 2017 is summarized in the table below:

NOTE 30 - Deferred tax liabilities

Deferred tax liabilities at 31 December 2017 amounted to 1,214,430 Euros and are referred mainly to the fiscal effects arising from temporary differences between the statutory income and taxable income.

NOTE 31 - Trade payables

Trade payables at 31 December 2017 amounted to 349,998,450 Euros with an increase of 53,766,509 Euros.

Detail is as follows:

Due to suppliers mainly refers to services from domestic suppliers. Due to subsidiary companies recorded a change of 10,370,427 Euros, and refers to professional services in connection to third party agreements with Reply S.p.A. Reply S.p.A. carries out commercial fronting activities for some of its major clients, whereas delivery is carried out by the operational companies.

Advance payments from customers include advances received from customers for contracts subcontracted to subsidiary companies, which at the balance sheet date were not yet completed.

The carrying amount of trade payables is deemed to be in line with its fair value.

NOTE 32 - Other current liabilities

Detail is as follows:

Due to tax authorities mainly refers to payables due for withholding tax on employees and free lancers’ compensation.

Due to social security authorities is related to both Company and employees’ contribution payables.

Employee accruals mainly include payables to employees for remunerations due but not yet paid at year-end.

Due to subsidiary companies represents the liability on tax losses recorded by subsidiaries under national tax consolidation for 2017 and for the tax credits that subsidiaries transferred to Reply S.p.A as part of the tax consolidation.

The carrying amount of the item Other current liabilities is deemed to be in line with its fair value.

NOTE 33 - Provisions

The item Provisions amounting to 15,234,000 Euros is summarized as follows:

The item Provision for risks reflects the best estimate of contingent liabilities deriving from ongoing legal litigations, at 31 December 2017 an accrual of 3,000,000 euros was made.

The item Provision for losses on equity investments has been adjusted because of the impairment test related to the value of the equity investments.

NOTE 34 - Transactions with related parties

With reference to CONSOB communications no. DAC/RM 97001574 of 20 February 1997 and no. DAC/RM 98015375 of 27 February 1998 concerning relations with related parties, the economic and financial effects on Reply S.p.A.’s year ended 2017 Financial Statements related to such transactions are summarized below.

Transactions carried out by Reply S.p.A. with related parties are considered ordinary business and are carried out at normal market conditions.

Financial and business transactions among the Parent Company Reply S.p.A. and its subsidiaries and associate companies are carried out at normal market conditions.

Reply S.p.A. main economic and financial transactions

In accordance with Consob Resolution no. 15519 of 27 July 2006 and Consob communication no. DEM/6064293 of 28 July 2006, in the annexed tables herein, the Statement of income and the Statement of financial position reporting transactions with related parties separately, together with the percentage incidence with respect to each account caption has been provided.

Pursuant to art. 150, paragraph 1 of the Italian Legislative Decree n. 58 of 24 February 1998, no transactions have been carried out by the members of the Board of Directors that might be in potential conflict of interests with the Company.

NOTE 35 - Additional disclosure to financial instruments and risk management policies

Types of financial risks and corresponding hedging activities

Reply S.p.A. has determined the guide lines in managing financial risks. In order to maximize costs and the resources Reply S.p.A. has centralized all of the groups risk management. Reply S.p.A. has the task of gathering all information concerning possible risk situations and define the corresponding hedge.

As described in the section “Risk management”, Reply S.p.A. constantly monitors the financial risks to which it is exposed, in order to detect those risks in advance and take the necessary action to mitigate them.

The following section provides qualitative and quantitative disclosures on the effect that these risks may have upon the company.

The quantitative data reported in the following do not have any value of a prospective nature, in particular the sensitivity analysis on market risks, is unable to reflect the complexity of the market and its related reaction which may result from every change which may occur.

Credit risk

The maximum credit risk to which the company is theoretically exposed at 31 December 2017 is represented by the carrying amounts stated for financial assets in the balance sheet.

Balances which are objectively uncollectible either in part or for the whole amount are written down on a specific basis if they are individually significant. The amount of the write-down takes into account an estimate of the recoverable cash flows and the date of receipt, the costs of recovery and the fair value of any guarantees received. General provisions are made for receivables which are not written down on a specific basis, determined on the basis of historical experience. Refer to the note on trade receivables for a quantitate analysis.

Liquidity risk

Reply S.p.A. is exposed to funding risk if there is difficulty in obtaining finance for operations at any given point in time.

The two main factors that determine the company’s liquidity situation are on one side the funds generated by or used in operating and investing activities and on the other the debt lending period and its renewal features or the liquidity of the funds employed and market terms and conditions.

As described in the Risk management section, Reply S.p.A has adopted a series of policies and procedures whose purpose is to optimize the management of funds and to reduce the liquidity risk, as follows:

-

Centralizing the management of receipts and payments, where it may be economical in the context of the local civil, currency and fiscal regulations of the countries in which the company is present;

-

Maintaining an adequate level of available liquidity;

-

Monitoring future liquidity on the basis of business planning.

Management believes that the funds and credit lines currently available, in addition to those funds that will be generated from operating and funding activities, will enable the Group to satisfy its requirements resulting from its investing activities and its working capital needs and to fulfil its obligations to repay its debts at their natural due date.

Currency risk

Reply S.p.A. has a limited exposure to exchange rate risk; therefore, the company does not deem necessary hedging exchange rates.

Interest rate risk

Reply S.p.A. makes use of external funds obtained in the form of financing and invest in monetary and financial market instruments. Changes in market interest rates can affect the cost of the various forms of financing, including the sale of receivables, or the return on investments, and the employment of funds, causing an impact on the level of net financial expenses incurred by the company.

In order to manage these risks, the Reply S.p.A uses interest rate derivative financial instruments, mainly interest rate swaps, with the object of mitigating, under economically acceptable conditions, the potential variability of interest rates on the net result.

Sensitivity analysis

In assessing the potential impact of changes in interest rates, the company separates fixed rate financial instruments (for which the impact is assessed in terms of fair value) from floating rate financial instruments (for which the impact is assessed in terms of cash flows).

Floating rate financial instruments include principally cash and cash equivalents and part of debt.

A hypothetical, unfavorable and instantaneous change of 50 basis points in short-term interest rates at 31 December 2017 applied to floating rate financial assets and liabilities, operations for the sale of receivables and derivatives financial instruments, would have caused increased net expenses before taxes, on an annual basis, of approximately 643 thousand Euros.

This analysis is based on the assumption that there is a general and instantaneous change of 50 basis points in interest rates across homogeneous categories. A homogeneous category is defined on the basis of the currency in which the financial assets and liabilities are denominated.

fair value hierarchy levels

Evaluation techniques on three levels adopted for the measurement of fair value. Fair value hierarchy attributes maximum priority to prices quoted (not rectified) in active markets for identical assets and liabilities (Level 1 data) and the non-observable minimum input priority (Level 3 data). In some cases, the data used to assess the fair value of assets or liabilities could be classified on three different levels of the fair value hierarchy. In such cases, the evaluation of fair value is wholly classified on the same level of the hierarchy in which input on the lowest level is classified, taking account its importance for the assessment.

The levels used in the hierarchy are:

-

Level 1 inputs are prices quoted (not rectified) in markets active for identical assets and liabilities which the entity can access on the date of assessment;

-

Level 2 inputs are variable and different from the prices quoted included in Level 1 observable directly or indirectly for assets or liabilities;

-

Level 3 inputs are variable and not observable for assets or liabilities.

The following table presents the assets and liabilities which were assessed at fair value on 31 December 2017, according to the fair value hierarchical assessment level.

The fair value of Liabilities to minority shareholders and earn out was determined by Group management on the basis of the sales purchase agreements for the acquisition of the company’s shares and on economic parameters based on budgets and plans of the purchased company. As the parameters are not observable on stock markets (directly or indirectly) these liabilities fall under the hierarchy profile in level 3.

As at 31 December 2017, there have not been any transfers within the hierarchy levels.

NOTE 36 - Significant non-recurring transactions

Pursuant to Consob communication no. 6064293 of 28 July 2006, there were no significant non-recurring transaction during 2017.

NOTE 37 - Transactions resulting from unusual and/or abnormal operations